The iron condor options strategy is one of the most popular structures in retail options trading. It is also one of the most misunderstood — especially when applied to same-day expiration contracts where the math quietly turns against you.

This guide breaks down exactly how the iron condor options strategy works, why the risk-to-reward ratio is structurally adverse, how it compares to the iron butterfly and the standard butterfly, and what the data actually shows when you trade iron condors on SPX 0DTE contracts.

If you have been collecting premium with iron condors and wondering why your account is not growing — or worse, why one bad session erases a month of wins — this is the page that explains it.

What Is an Iron Condor Options Strategy?

An iron condor is a four-leg options strategy that collects premium by selling an out-of-the-money call spread and an out-of-the-money put spread simultaneously. You are betting that price stays inside a range between your two short strikes until expiration.

The structure:

- Sell an OTM put — collect premium on the downside

- Buy a further OTM put — cap your downside risk

- Sell an OTM call — collect premium on the upside

- Buy a further OTM call — cap your upside risk

The credit you receive is your maximum profit. The width of either spread minus the credit is your maximum loss. On paper, it looks elegant — profit if the market stays still, defined risk on both sides. In practice, the iron condor options strategy has a structural problem that most traders discover too late.

The Iron Condor Options Strategy Risk-to-Reward Problem

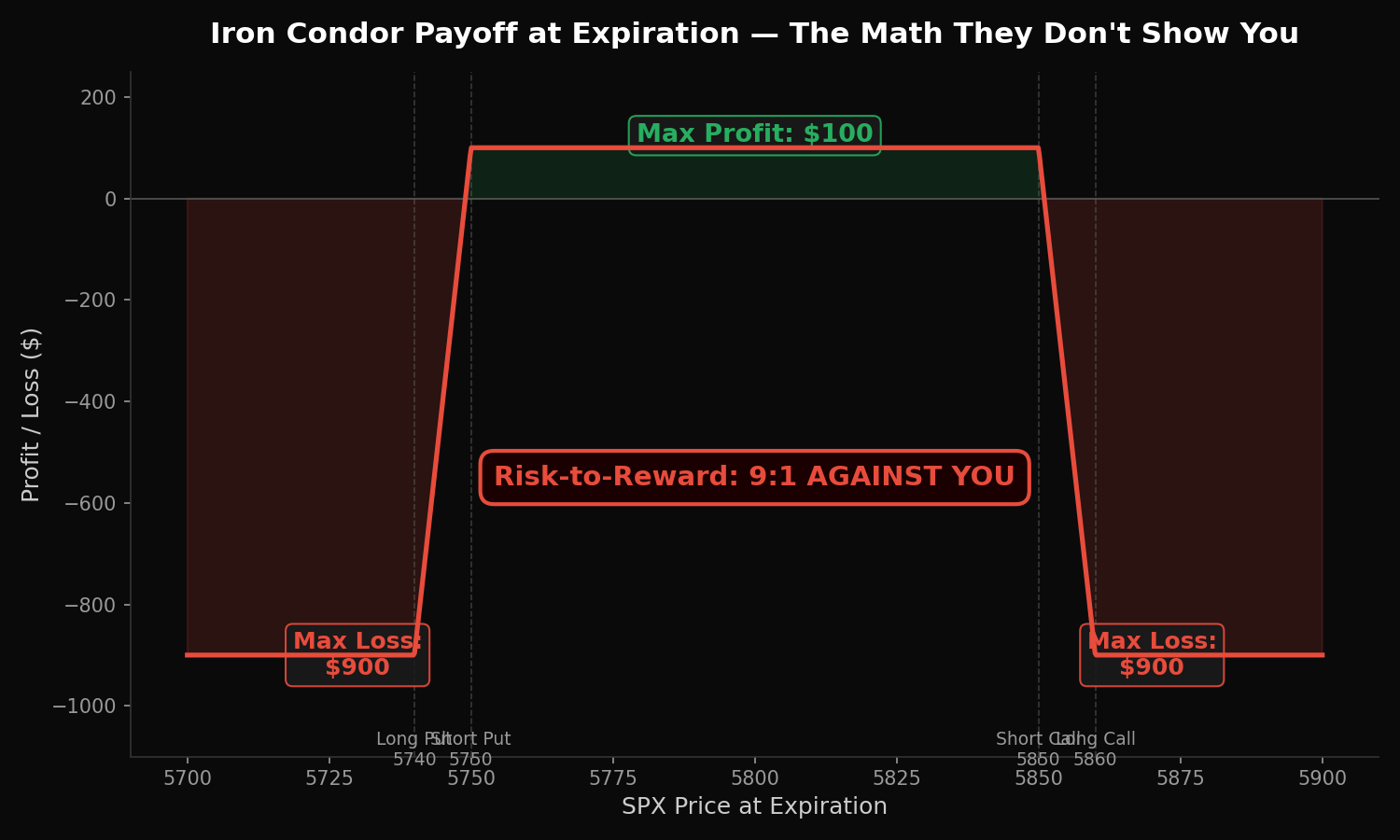

Here is a typical iron condor on SPX 0DTE:

- Sell the 5750 put / Buy the 5740 put (10-wide put spread)

- Sell the 5850 call / Buy the 5860 call (10-wide call spread)

- Net credit received: $1.00 ($100 per contract)

- Maximum loss on either side: $9.00 ($900 per contract)

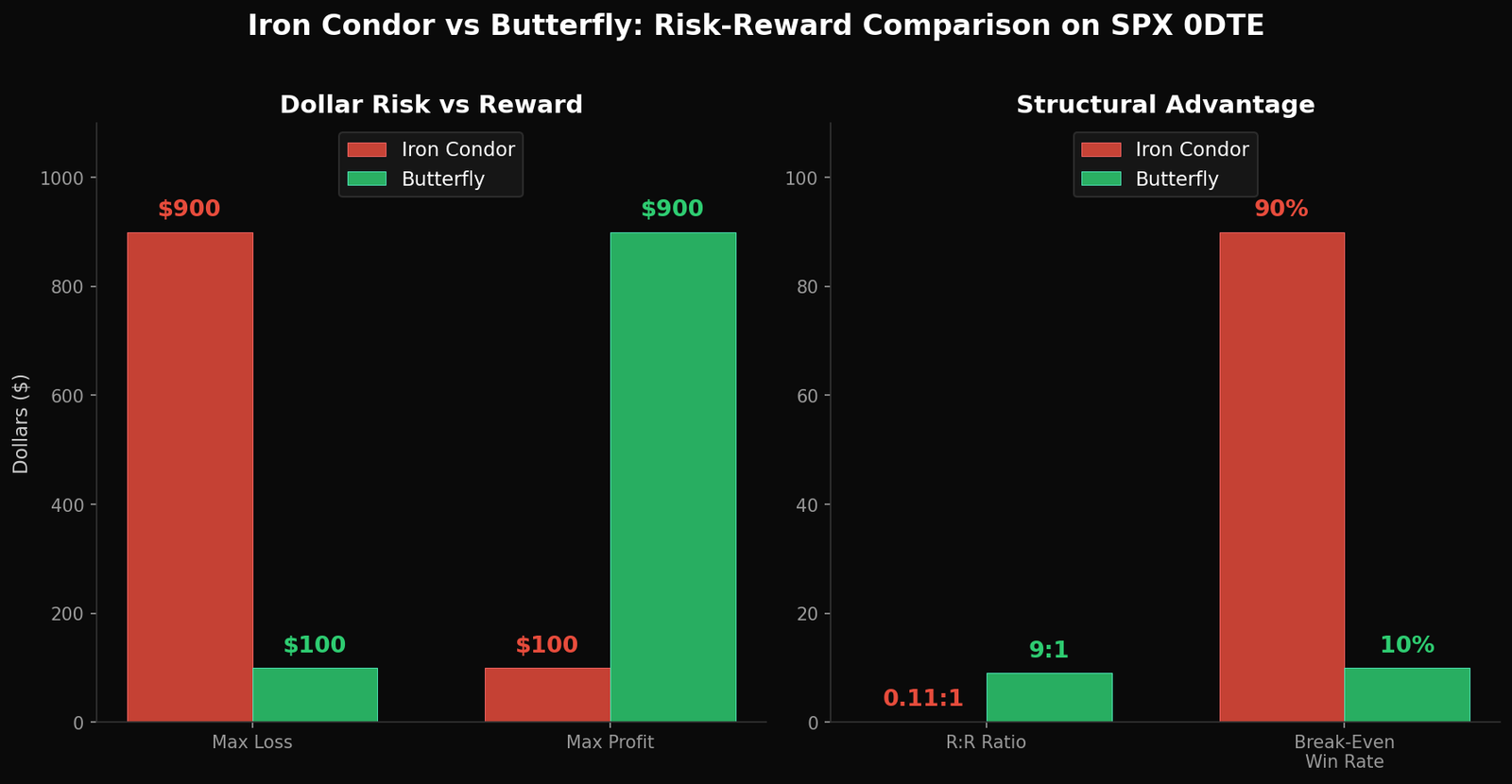

That is a 9:1 adverse risk-to-reward ratio. You risk $900 to make $100.

To break even over time with this iron condor options strategy, you need to win approximately 90% of your trades. Not 70%. Not 80%. Ninety percent. One loss wipes out nine winners. Two consecutive losses wipe out eighteen winners.

This is not a risk management problem you can solve with better entries. It is a structural deficiency built into the strategy itself. The iron condor options strategy rewards you with a small, frequent profit while exposing you to an infrequent but catastrophic loss. That is the textbook definition of negative skew — and negative skew compounds against you over time.

Why the Iron Condor Options Strategy Fails on 0DTE

The iron condor options strategy requires one thing above all else: a range-bound market. Price must stay between your short strikes for the entire session. On longer-dated options, this is plausible — you have weeks for the market to oscillate within a range and for theta to decay your short options.

On same-day expiration contracts, three things work against the iron condor:

Gamma is at its peak. On the final day of an option’s life, gamma — the rate at which delta changes — is at its maximum. Small price moves create large swings in option value. A 15-point SPX move that barely registers on a 30-day option can blow through an iron condor’s short strike in minutes on a 0DTE contract. The iron condor options strategy was designed for low-gamma environments. Same-day expiration is the highest-gamma environment that exists.

Intraday regime shifts are common. Markets do not stay in one mode all day. A session that opens in a grinding, range-bound mode can shift to a trending mode after an economic release, a VIX spike, or a dealer gamma flip. The iron condor has no mechanism to adapt to this. Once price breaches a short strike, the loss accelerates toward maximum.

There is no time to recover. On a 45-day iron condor, if price moves against you early, there are weeks remaining for it to come back. On a 0DTE iron condor, if price breaches your short strike at 11:00 AM, you have five hours of accelerating gamma working against you. The position does not recover. It deteriorates.

Iron Condor vs Iron Butterfly — What Actually Changes

Some traders hear that iron condors are problematic and switch to iron butterflies, assuming the centered structure fixes the issue. It does not solve the core problem.

An iron butterfly sells both the put and the call at the same strike (at the money) and buys wings on either side. Because the at-the-money options carry more premium, the credit collected is larger — but so is the risk if price moves away from the center.

The key differences:

- Iron butterfly — larger credit, narrower profit zone, maximum profit only if SPX settles exactly at the short strike. Higher probability of partial loss.

- Iron condor — smaller credit, wider profit zone, maximum profit if SPX settles anywhere between the short strikes. Lower win amount per trade.

Both strategies share the same fundamental flaw: they are short gamma, short volatility structures that profit from stasis and suffer from movement. On a day where SPX moves 30+ points — which happens regularly — both structures produce losses that dwarf their typical wins.

The iron condor vs iron butterfly choice is a rearrangement of the same adverse math. Neither solves the structural problem. Both are premium collection strategies where the risk is larger than the reward, and both require an unrealistically high win rate to compound positively over time.

The Butterfly Alternative — Inverted Risk-to-Reward

A standard butterfly spread inverts everything about the iron condor’s risk profile.

Instead of collecting a small credit and risking a large loss, you pay a small debit and position for a large gain. A typical SPX 0DTE butterfly costs $0.40-$1.50 per contract ($40-$150) with a maximum return of $9.00-$10.00 per contract ($900-$1,000).

That is a 9:1 favorable risk-to-reward ratio. The exact inverse of the iron condor.

To break even with butterflies, you need to win roughly 10-15% of your trades — not 90%. In practice, a well-structured butterfly strategy using regime-aware width selection wins 45-65% of the time. That margin between the required win rate and the actual win rate is where the edge lives.

The butterfly thrives in the same environment that kills the iron condor:

- Amplified gamma — small price moves toward the body of the butterfly produce outsized gains. The same gamma that destroys iron condors accelerates butterfly profits.

- Accelerated theta — the butterfly benefits from time decay on its short legs. On 0DTE, this decay happens in hours, not weeks, concentrating the profit potential into a single session.

- Defined risk — your maximum loss is the debit paid. No margin expansion. No assignment risk on SPX (European-style exercise). No overnight exposure.

This is not a marginal improvement. The iron condor options strategy risks $900 to make $100. The butterfly risks $100 to make $900. On a 0DTE contract where gamma is amplified and regime shifts are common, the butterfly’s structural advantage is not theoretical. It is the measurable difference between a strategy that compounds and one that quietly bleeds.

What the Performance Data Actually Shows

These are not hypothetical comparisons. This is what the structural data shows across live 0DTE trading sessions:

Iron condor typical performance:

- Win rate: 75-85% (high, but not high enough)

- Average win: $80-$120 (credit collected minus commissions)

- Average loss: $700-$900 (near max loss when breached)

- Break-even win rate required: ~90%

- Result: slow bleed punctuated by catastrophic drawdowns

Butterfly typical performance:

- Win rate: 45-65% depending on VIX regime

- Average win: $180-$500+ (asymmetric payoffs on runners)

- Average loss: $40-$150 (the debit paid)

- Break-even win rate required: ~10-15%

- Result: consistent small losses offset by occasional large wins — positive skew that compounds

The iron condor feels like it is working because you win most of the time. The butterfly feels uncomfortable because you lose often. But the account balance tells the opposite story. One strategy produces a positively skewed return distribution. The other produces a negatively skewed one. Over hundreds of trades, skew wins. Always.

The Reverse Iron Condor — A Better Premium Structure

If you are committed to trading a condor-shaped structure, the reverse iron condor deserves attention. Instead of selling the inner strikes and buying the outer strikes, you flip it — buy the inner strikes and sell the outer strikes.

This creates a debit structure that profits from a large move in either direction. You pay a premium upfront (defined risk) and profit if SPX moves beyond either wing by expiration.

The reverse iron condor shares the butterfly’s structural advantage: small risk, large potential reward. It is essentially a strangle with defined risk — you are long volatility instead of short volatility. On a 0DTE session where a regime shift or trend day occurs, the reverse iron condor captures the move that would have destroyed a standard iron condor.

The trade-off is that you lose on range-bound days. But when the debit is $100-$200 and the potential return is $800-$900, the math works in your favor over time — the opposite of the standard iron condor options strategy.

Common Iron Condor Options Strategy Mistakes

These patterns appear repeatedly in the trading records of iron condor traders who eventually quit:

Widening the wings to collect more credit. This increases the credit by a small amount while increasing the maximum loss substantially. A 20-wide iron condor on SPX does not collect twice the premium of a 10-wide — but the max loss doubles. The risk-to-reward ratio gets worse, not better.

Adjusting the losing side. When price approaches a short strike, many iron condor traders roll the threatened side further out. This locks in a partial loss on the original position, opens a new risk exposure, and increases overall capital at risk. Rolling is not risk management. It is loss deferral with compounding risk.

Ignoring the VIX regime. An iron condor placed when VIX is at 28 has a fundamentally different probability of success than one placed at VIX 14. High-volatility environments produce larger intraday ranges, making it far more likely that price breaches a short strike. The iron condor options strategy demands low-volatility conditions — and many traders do not check the regime before entering.

Counting wins instead of measuring R-multiples. An 85% win rate sounds exceptional until you calculate the R-multiple: winning $100 eighty-five times ($8,500) and losing $900 fifteen times ($13,500). Net result: -$5,000. The win rate was never the metric that mattered. Risk-adjusted return was.

Sizing by contract count instead of risk. Selling 10 iron condors because “the premium looks good” means risking $9,000 on a single session. If that session produces a trending move, the loss is not an inconvenience. It is a career event. Position sizing should always be denominated in risk units, never in contract count.

Frequently Asked Questions

What is an iron condor options strategy?

An iron condor is a four-leg options strategy that sells an out-of-the-money put spread and call spread simultaneously, collecting premium. Maximum profit occurs if price stays between the short strikes at expiration. Maximum loss occurs if price moves beyond either wing. The strategy has an adverse risk-to-reward ratio — typically risking $800-$900 to collect $100-$200 in premium.

What is the difference between an iron condor and an iron butterfly?

An iron condor sells strikes away from the current price on both sides, creating a wide profit zone with a smaller credit. An iron butterfly sells both options at the same strike (at the money), collecting a larger credit but with a narrower profit zone. Both are short-volatility strategies with adverse risk-to-reward ratios. The choice between them is a trade-off between probability and payoff — neither solves the structural risk problem.

Why do iron condors fail on 0DTE options?

Iron condors require range-bound conditions for the entire trading session. On 0DTE contracts, gamma is at its peak, meaning small price moves cause large changes in option value. Intraday regime shifts can turn a grinding session into a trending one within minutes. When this happens, the iron condor’s short strike is breached and the loss accelerates toward maximum — with no time remaining for recovery.

What is a reverse iron condor?

A reverse iron condor flips the standard structure — you buy the inner strikes and sell the outer strikes, creating a debit position that profits from large moves in either direction. Instead of collecting premium and hoping price stays still, you pay a small premium and profit from volatility. The risk-to-reward ratio is favorable: risk the debit paid, profit from movement. It is structurally aligned with 0DTE gamma dynamics rather than fighting them.

Are butterfly spreads better than iron condors for 0DTE trading?

For same-day expiration on SPX, butterfly spreads offer a structurally superior risk-to-reward profile. A butterfly risks $40-$150 with potential returns of 5-25x the debit paid. An iron condor risks $800-$900 to collect $100-$200 in premium. The butterfly requires a 10-15% win rate to break even while the iron condor requires approximately 90%. Over hundreds of trades, the butterfly’s positive skew compounds favorably while the iron condor’s negative skew compounds against you.

Choose Structures That Survive Their Worst Day

The iron condor options strategy is not a bad strategy in all contexts. On longer-dated options in low-volatility environments, it can produce consistent income. But on 0DTE SPX contracts — where gamma is amplified, regime shifts happen intraday, and there is no time for recovery — the iron condor’s structural weaknesses are exposed in real time.

The question is not whether you can win with iron condors. You can. You will win most of the time. The question is whether your wins are large enough to survive the losses. With a 9:1 adverse risk-to-reward ratio, the math says no.

At Fly on the Wall, structural awareness comes first. Before every session, we surface the regime context, dealer positioning, and gamma exposure that determine which strategies have a structural edge — and which ones are fighting the environment. Start with the Observer for daily structural analysis and market positioning tools. Step up to Activator for full execution tools, GEX overlay, and weekly coaching. Or go all-in with Navigator for daily direct coaching with Ernie. Compare all plans here.