IV crush is the single most destructive force in options trading for anyone selling premium. It is the sudden collapse of implied volatility — and with it, the collapse of option prices — that occurs after a known event passes. For traders on the wrong side of this collapse, IV crush erases profits, amplifies losses, and turns high-probability trades into losing positions in minutes. No warning. No recovery. No second chance.

The mechanics are straightforward. Options are priced partly on implied volatility — the market’s estimate of how much the underlying will move. Before an event like earnings, FOMC, or a major economic release, implied volatility rises because the outcome is uncertain. After the event passes, uncertainty drops, implied volatility collapses, and every option loses value — sometimes dramatically. This is IV crush.

This guide explains what IV crush is, how it works mechanically, why it devastates iron condors and credit spreads, and how structural traders using 0DTE butterfly spreads avoid it entirely. If you trade SPX options around events, understanding IV crush is not optional — it is the difference between a strategy that compounds and one that quietly bleeds.

What Is IV Crush in Options?

IV crush is the rapid decline in implied volatility — and therefore option premiums — that occurs when uncertainty resolves. The term describes the speed and magnitude of the drop: implied volatility does not ease down gradually. It crushes.

Implied volatility represents the market’s forecast of future price movement, expressed as an annualized percentage. When traders expect a large move — before earnings, before an FOMC decision, before a CPI release — they bid up option prices. This demand inflates implied volatility. The moment the event passes and the outcome is known, that demand evaporates. Implied volatility drops, and every option contract reprices lower.

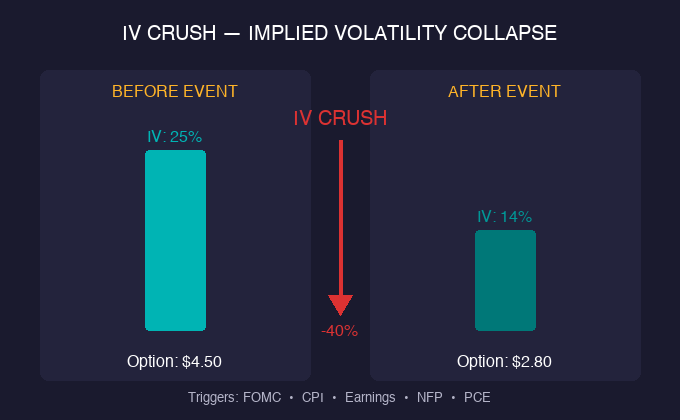

A concrete example: SPX at 5800 before a morning CPI release. Implied volatility on 0DTE options might sit at 22% — elevated because the number could move the market in either direction. The CPI prints, the market reacts with a 15-point move, and implied volatility drops to 14% within 30 minutes. Every option — calls and puts at every strike — loses value from the volatility component alone, regardless of direction. An option worth $4.50 before the print might be worth $2.80 after, even if the underlying moved in your favor.

That gap between $4.50 and $2.80 is IV crush. The directional move helped, but the volatility collapse took more than it gave.

Why Implied Volatility Collapses After Events

IV crush is not random. It follows a predictable pattern tied to the resolution of uncertainty.

Options pricing models use implied volatility as a key input. Higher implied volatility means wider expected move ranges, which means more expensive options. When uncertainty exists about an upcoming event, the market prices a wider range of possible outcomes. Options become expensive because the potential magnitude of the move is unknown.

The moment the event occurs, two things happen simultaneously. First, the range of possible outcomes narrows to the actual outcome. Second, the time until the next uncertainty event extends — there is nothing left to price in. Both effects compress implied volatility.

This is why IV crush is most severe around binary events. Earnings, FOMC rate decisions, CPI releases, and NFP prints are the classic triggers. The VIX — which measures implied volatility on the S&P 500 — often drops 2 to 5 points in a single session after an FOMC decision, even if the decision itself was contentious.

The severity of IV crush depends on how elevated implied volatility was before the event. If IV expanded from 15% to 25% ahead of a print, the crush back to 15% represents a 40% decline in the volatility component of every option. The more inflated the premium, the harder it falls.

How IV Crush Destroys Iron Condors and Credit Spreads

This is where IV crush becomes dangerous for the most popular strategies in options trading.

Iron condors and credit spreads profit from selling premium. The trader collects a credit upfront and hopes that the options expire worthless or lose value. On the surface, IV crush should help these strategies — if all options lose value, the premium seller profits. This is the logic that attracts traders to selling options around events.

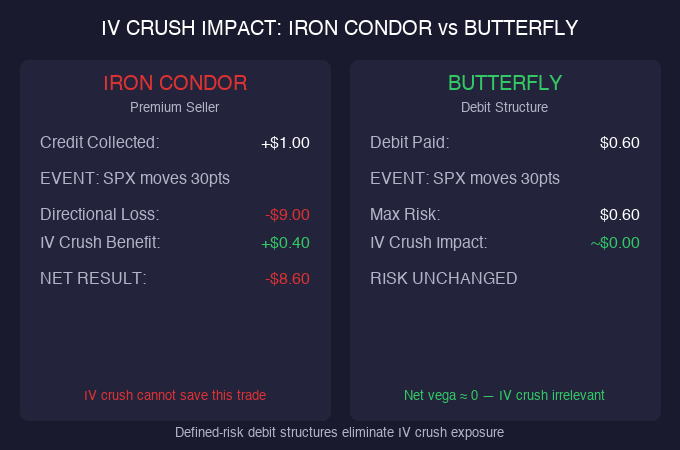

The problem is timing and magnitude. An iron condor placed before an event carries maximum exposure to the directional move that triggers the crush. A 30-point SPX move through the short strike of an iron condor creates a loss that dwarfs any benefit from the subsequent volatility collapse. The crush helps the position — but only after the directional damage has already been done.

Credit spreads face the same structural problem. A bull put spread sold before CPI collects a credit of $1.00 and risks $9.00. If CPI prints hot and SPX drops 40 points through the short put strike, the spread goes to maximum loss. IV crush occurs simultaneously, but the directional move already killed the trade. The volatility collapse is a consolation prize for a trade that lost its maximum amount.

The math is not in your favor. Premium sellers need IV crush to happen without a directional breach. But the events that cause the largest IV crush are exactly the events that produce the largest directional moves. The two are structurally correlated — you cannot have one without the other. This is why selling premium into known events has a deceptive win rate. The strategy wins on small events and loses catastrophically on large ones — precisely the negatively skewed distribution that compounds against you over hundreds of trades.

How Butterfly Traders Avoid IV Crush Entirely

Butterfly spreads sidestep IV crush — not because they are immune to volatility changes, but because their structure makes the volatility component irrelevant to the risk profile.

Your maximum risk is the debit paid. A butterfly costs $0.60 to enter. That is the total risk — $60 per contract. Whether implied volatility is at 14% or 28% after the event, the maximum loss is still $0.60. IV crush cannot increase your risk because there is no short premium exposure to expand against you.

Butterflies benefit from price convergence, not premium collection. A butterfly profits when the underlying settles near the body strike at expiration. This is a directional and structural outcome — it has nothing to do with whether implied volatility expanded or collapsed. A butterfly placed at SPX 5800 that expires with SPX at 5802 will reach near-maximum value regardless of what happened to implied volatility during the session.

The vega exposure is minimal and balanced. A butterfly has two long options and two short options. The long wings and short body partially offset each other’s vega exposure. The net vega of a butterfly is close to zero — meaning the position is largely insensitive to changes in implied volatility. This is the structural reason butterflies are not affected by IV crush.

On 0DTE contracts, vega matters even less. With hours until expiration, gamma dominates the Greeks. Implied volatility changes have almost no effect on option prices when expiration is minutes away. The physics that makes IV crush devastating for premium sellers simply does not apply to defined-risk debit structures on same-day expiration.

The 0DTE Factor — Why Volatility Crush Matters Less Than You Think

On same-day expiration contracts, IV crush exists but operates differently than on longer-dated options.

The time frame is compressed. A weekly or monthly option might experience IV crush over a full trading day. On 0DTE, the same compression happens in minutes. An 8:30 AM economic release on SPX will crush implied volatility on 0DTE options before 9:00 AM. By the time the regular session opens at 9:30, the crush is already complete.

Gamma dominates vega. On the final day of an option’s life, gamma is at its peak and vega is near zero. This means option prices respond almost entirely to directional movement and time decay — not to implied volatility changes. A 10-point SPX move on 0DTE changes option prices more than a 5-point drop in implied volatility. For butterfly traders, this means the trade is being driven by price action and theta, not by volatility dynamics.

The practical implication. If you are trading 0DTE butterflies, IV crush is not your primary concern. Price convergence near the body and theta decay are what drive your P&L. However, if you are selling premium on 0DTE around events — iron condors, credit spreads, naked options — IV crush does not help you enough to offset the gamma exposure risk. The directional move kills the position before the volatility drop can help it.

How to Spot Volatility Crush Before It Happens

IV crush is predictable. The conditions that produce it are known in advance.

Check the economic calendar. FOMC decisions, CPI, NFP, PCE, and earnings are the primary triggers. If one of these events falls during your trading session, implied volatility will be elevated before the release and will compress after. This is not speculation — it is the mechanical consequence of uncertainty resolving.

Compare implied volatility to realized volatility. If implied volatility is significantly above the 20-day realized volatility — a gap of 5 or more percentage points — the market is pricing an event. That gap will close when the event passes. The wider the gap, the more severe the potential IV crush.

Watch the expected move. An unusually wide expected move relative to recent session ranges signals inflated implied volatility. If the expected move on SPX is 45 points but the average recent daily range is 25 points, the excess is event premium that will disappear after the event resolves.

Monitor the VIX term structure. When the front-month VIX is higher than the second-month VIX — a condition called backwardation — the market is pricing near-term uncertainty. After the event resolves, the term structure will normalize. That normalization is IV crush expressed across the volatility surface.

Common Mistakes When Trading Around Volatility Events

Selling premium specifically to capture IV crush. This is the most popular mistake in options trading. Traders see elevated implied volatility before an event and sell options to profit from the expected crush. The logic seems sound — until the event produces a large directional move that breaches the short strike. The crush happens, but the directional loss is larger. Over many iterations, this produces a negatively skewed distribution that works against you.

Assuming IV crush means all options lose value equally. IV crush affects at-the-money options most severely because they have the highest vega. Out-of-the-money options have lower vega and are less affected. This means a butterfly — which is net-long out-of-the-money options and net-short at-the-money options — can actually benefit slightly from IV crush in some configurations.

Ignoring IV crush on multi-day holds. If you hold options overnight through an event, IV crush will affect your position at the open. A butterfly purchased on Monday for a Wednesday FOMC decision will experience IV crush Wednesday afternoon regardless of the directional outcome. For 0DTE traders, this is irrelevant — there is no overnight hold. But for swing traders, event-driven IV crush is a position-sizing consideration.

Confusing IV crush with theta decay. IV crush and time decay are different mechanisms. Theta decay is the predictable, daily erosion of time value. IV crush is the sudden, event-driven compression of implied volatility. Both reduce option prices, but theta decay is continuous and expected while IV crush is discrete and tied to specific catalysts. On 0DTE contracts, theta decay is the dominant force — do not confuse the two when analyzing your position’s behavior.

Frequently Asked Questions

What is IV crush in options?

IV crush is the rapid decline in implied volatility — and therefore option premiums — that occurs after a known event such as earnings, FOMC decisions, or economic data releases. Before the event, uncertainty drives implied volatility higher. After the event resolves, uncertainty collapses and every option loses value from the volatility component. The term describes the speed of the decline — implied volatility does not ease down, it crushes.

How does IV crush affect iron condors?

IV crush theoretically helps premium sellers because all options lose value. However, the events that cause IV crush also produce the largest directional moves. A 30-point SPX move through the short strike of an iron condor creates a loss that dwarfs any benefit from the subsequent volatility collapse. The directional damage happens simultaneously with the crush, making it impossible to capture the volatility benefit without bearing the full directional risk.

Do butterflies get affected by IV crush?

Butterflies are largely immune to IV crush. The structure has near-zero net vega because the long wings and short body offset each other’s volatility exposure. The maximum risk is the debit paid — IV crush cannot increase that risk. On 0DTE contracts where gamma dominates and vega is near zero, implied volatility changes are even less relevant to the butterfly’s value.

When does IV crush happen?

IV crush occurs immediately after a binary event resolves — typically within minutes to an hour. Common triggers include earnings announcements, FOMC rate decisions, CPI releases, NFP prints, and PCE data. The crush is most severe when implied volatility was most elevated before the event. On 0DTE, pre-market economic releases crush implied volatility before the regular session opens.

How do you avoid IV crush?

Use defined-risk debit structures like butterfly spreads instead of selling premium. Butterflies have near-zero vega and a maximum loss equal to the debit paid — IV crush cannot expand your risk. Alternatively, trade after the event passes when implied volatility has already compressed. If you must sell premium, avoid holding short positions through known binary events where the largest directional moves coincide with the largest volatility crush.

Trade Structure, Not Volatility

IV crush is not a risk for traders who understand structure. It is a risk for traders who collect premium and hope that volatility collapses before direction destroys them. That hope-based approach produces a negatively skewed return distribution — small wins, occasional catastrophic losses — that compounds against you over time.

At Fly on the Wall, the structural approach removes IV crush from the equation entirely. The butterfly structure has near-zero vega, defined risk, and profits from price convergence — not from volatility behavior. The expected value zone, the GEX overlay, and the regime-based width selection give you the structural framework to trade with precision regardless of what implied volatility does before, during, or after an event.

Start with the Observer for daily structural analysis and the tools that surface the expected move and market positioning before every session. Step up to Activator for full execution tools, real-time GEX overlay, and weekly coaching. Or go all-in with Navigator for daily direct coaching with Ernie. Compare all plans here.