The iron butterfly is the most misunderstood structure in options trading. It looks like an iron condor. It trades like a butterfly. And for 0DTE traders who understand when to deploy it, the iron butterfly delivers a risk-to-reward profile that neither structure achieves on its own. Defined risk. Centered precision. Maximum theta decay concentrated into the body where price is most likely to settle.

Most traders encounter the iron butterfly as a textbook definition and move on. That is a mistake. The iron butterfly is a structural tool — not a theoretical curiosity — and it occupies a specific role in the options toolkit that no other spread can fill. It is the centered convergence play for sessions where price is expected to stay pinned near a single level, and it does this with a credit collected at entry rather than a debit paid.

This guide explains what the iron butterfly is, how it differs from iron condors and standard butterfly spreads, when to use it on SPX options, and how it fits into a structural 0DTE trading approach built around expected move and regime analysis.

What Is an Iron Butterfly in Options Trading?

An iron butterfly is a four-leg options strategy that combines a short straddle with protective wings. The construction is precise:

- Sell one at-the-money call — the upper body

- Sell one at-the-money put — the lower body

- Buy one out-of-the-money call — the upper wing

- Buy one out-of-the-money put — the lower wing

All four legs share the same expiration date. The short call and short put are at the same strike — the body — and the long call and long put are equidistant above and below.

The result is a credit spread that profits most when the underlying settles exactly at the body strike at expiration. The maximum profit is the credit received. The maximum loss is the width of one wing minus the credit — and that loss is capped. No margin expansion. No assignment risk on SPX (European-style, cash-settled). The iron butterfly is particularly effective on SPX options where deep liquidity supports tight fills on all four legs.

A concrete example: SPX at 5800. Sell the 5800 call and 5800 put. Buy the 5810 call and 5790 put. If the credit received is $7.00, the maximum profit is $700 per contract if SPX settles at exactly 5800. The maximum loss is $10.00 minus $7.00 = $3.00 ($300 per contract) — and that only occurs if SPX moves beyond either wing at expiration.

Structural Differences From the Iron Condor

The iron butterfly and the iron condor are structural cousins — both are four-leg credit spreads with defined risk. But they serve fundamentally different purposes.

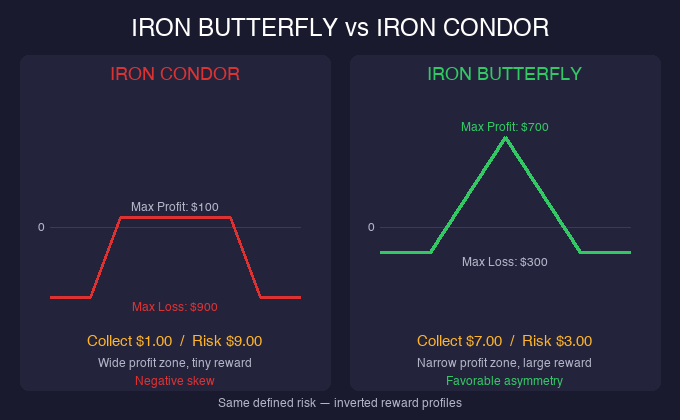

An iron condor has a wide profit zone and a narrow reward. The short strikes are spread apart, creating a range where the trade profits. The credit collected is small relative to the risk because the probability of staying inside the range is high. A typical iron condor collects $1.00 and risks $9.00. It wins often but loses big.

An iron butterfly has a narrow profit zone and a larger reward. The short strikes are at the same price — the body — so the maximum profit zone is a single point. But the credit collected is much larger relative to the risk because the short straddle at the body commands significant premium. A typical iron butterfly collects $7.00 and risks $3.00. It wins less often but the reward-to-risk ratio is inverted in your favor.

The risk profiles are inversions of each other. The iron condor is a high-probability, low-reward trade with negative skew. The iron butterfly is a moderate-probability, high-reward trade with more favorable asymmetry. For traders who understand that implied volatility and gamma work against wide premium-selling structures on 0DTE, the iron butterfly represents a structural improvement.

Iron Butterfly vs Butterfly Spread — Credit vs Debit

The iron butterfly and the standard butterfly spread produce nearly identical payoff diagrams at expiration. The difference is in how you enter the trade.

A butterfly spread is a debit trade. You pay $0.60 upfront and can make $9.40 if SPX settles at the body. Your maximum risk is the debit paid. The trade starts at a loss and profits as price converges on the body.

An iron butterfly is a credit trade. You collect $7.00 upfront and can keep the full credit if SPX settles at the body. Your maximum risk is the wing width minus the credit. The trade starts at a profit and loses value as price moves away from the body.

At expiration, the payoff is identical. Both structures make maximum money at the body and lose money at the wings. The difference is psychological and mechanical. The butterfly requires the underlying to converge — you are waiting for the trade to work. The iron butterfly starts profitable and you are managing against adverse movement. Some traders prefer the iron butterfly specifically because collecting a credit feels like a head start.

The practical distinction on 0DTE. On same-day expiration contracts, the debit butterfly is generally preferred because the debit is small ($40 to $150), the maximum risk is the amount paid, and there is no short premium exposure to manage. The iron butterfly collects more premium but requires margin for the short straddle component. For traders with smaller accounts or those who prefer the simplicity of defined-risk debit trades, the standard butterfly is the cleaner structure.

When to Use an Iron Butterfly on SPX

The iron butterfly is not an every-session trade. It is a specific tool for specific conditions.

Low-volatility, range-bound sessions. When the VIX is below 17 and the expected move is compressed, price tends to settle near the open. These Zombieland sessions are where the iron butterfly thrives. The body at the current price captures maximum theta decay while the narrow wings are unlikely to be breached.

High-GEX pinning environments. When gamma exposure data shows a strong positive GEX level at a specific strike, dealer hedging tends to pin price near that level. An iron butterfly with the body at the high-GEX strike leverages this structural force. Price is being pulled toward your maximum profit point by the mechanics of the market itself.

After-event compression. Following a major economic release or FOMC decision, implied volatility collapses and the session often enters a grinding, range-bound character. An iron butterfly placed after the initial move and volatility compression capitalizes on the reduced range for the remainder of the session.

When NOT to use an iron butterfly. Trending sessions, negative gamma environments, and VIX above 24 are poor conditions. If price is moving directionally with momentum, the body of the iron butterfly will be breached quickly and the trade moves to maximum loss. The iron butterfly requires price convergence — it has no edge in trending markets.

Width Selection by VIX Regime

Width selection follows the same regime logic that governs all structural butterfly trading.

Zombieland (VIX 17 or below). Use a 10-wide iron butterfly. The compressed range means price is unlikely to travel far from the body. A 10-wide structure on SPX at 5800 means buying the 5790 put and the 5810 call as wings. The credit collected will be $6.00 to $8.00, with a maximum risk of $2.00 to $4.00.

Goldilocks (VIX 17 to 24). Use a 15-wide iron butterfly. This is the most common regime for iron butterflies — enough movement to create opportunity but not enough to routinely breach the wings. Credit collected: $8.00 to $11.00. Maximum risk: $4.00 to $7.00.

Elevated (VIX 24 to 32). Consider a 20-wide iron butterfly — or switch to a directional debit butterfly instead. At elevated volatility, the credit collected is large but the probability of price remaining near the body decreases. The iron butterfly becomes less reliable in these conditions.

Chaos (VIX above 32). Do not trade iron butterflies. The range expansion makes the narrow profit zone a losing proposition. Not every session deserves this structure. Use wider debit butterflies or sit out entirely.

Trade Management — Profit Targets and Exits

The iron butterfly starts at maximum profit and decays as price moves away from the body. Management is about recognizing when to close and lock in the credit — not about waiting for a target.

Close at 50% to 75% of maximum credit retained. If the iron butterfly collected $7.00, close the trade when the position is worth $1.75 to $3.50. This means you keep $3.50 to $5.25 of the credit. Do not hold for the full $7.00 — the probability of SPX settling at exactly 5800 is low, and the risk-reward of holding for the last dollar of profit is poor.

Time-based exit. If less than 90 minutes remain in the session and the trade is profitable, close it. Gamma accelerates in the final hour and a sudden 10-point move can flip a profitable iron butterfly to a loser. Take the profit that the session has given.

Exit on structural change. If the VIX spikes mid-session, if a gamma flip occurs, or if a news event triggers a directional move, close the trade regardless of current profit or loss. The structural thesis that justified the iron butterfly — range-bound, low-volatility, pinning — no longer holds. Respect the change.

Maximum loss is defined. If price breaches the wings and stays there, the iron butterfly loss is the wing width minus the credit. This is known at entry. There is no need for a stop loss — the structure defines the risk. Let the iron butterfly work or let it expire. Do not add legs or roll the position on 0DTE.

Frequently Asked Questions

What is an iron butterfly in options?

An iron butterfly is a four-leg options strategy that combines selling a straddle at one strike (the body) with buying protective wings above and below. It collects a credit at entry and profits most when the underlying settles at the body strike at expiration. The maximum risk is the wing width minus the credit received. It is a defined-risk, credit-based structure.

What is the difference between an iron butterfly and an iron condor?

An iron condor has separate short strikes creating a wide profit zone with a small credit (collect $1, risk $9). An iron butterfly has both short strikes at the same price, creating a narrow profit zone with a large credit (collect $7, risk $3). The iron condor wins more often but has worse risk-to-reward. The iron butterfly wins less often but has inverted, more favorable asymmetry.

Is an iron butterfly the same as a butterfly spread?

The payoff at expiration is nearly identical. The difference is entry mechanics — a butterfly spread pays a debit and an iron butterfly collects a credit. The butterfly risks the debit paid while the iron butterfly risks the wing width minus the credit. For 0DTE trading, the debit butterfly is generally preferred for its simplicity and lower margin requirement.

When should you trade an iron butterfly?

Iron butterflies work best in low-volatility, range-bound sessions where price is expected to settle near a single level. Ideal conditions include VIX below 17 (Zombieland regime), strong positive gamma exposure pinning at a specific strike, and post-event compression where implied volatility has already collapsed. Avoid iron butterflies in trending or high-volatility environments.

Can you trade iron butterflies on SPX 0DTE?

Yes. SPX is the preferred instrument because it is cash-settled (no assignment risk), European-style (no early exercise), and has the deepest liquidity for same-day expiration contracts. The iron butterfly collects significant premium on 0DTE due to elevated gamma, but the debit butterfly is often the simpler structure for same-day trading because it requires less margin and has a cleaner risk profile.

Use the Right Structure for the Right Session

The iron butterfly is not better or worse than a standard butterfly or an iron condor. It is a different tool. It belongs in sessions where price convergence is the highest-probability outcome — low-volatility grinds, high-GEX pinning, and post-event compression. Using it outside those conditions is forcing a structure onto a market that does not support it.

At Fly on the Wall, the structural read tells you which tool to deploy. The GEX overlay shows where dealer hedging pins price. The expected value zone shows the range where convergence is most likely. The VIX regime determines your width. The structure follows the environment — not the other way around.

Start with the Observer for daily structural analysis and the tools that surface the expected move and market positioning before every session. Step up to Activator for full execution tools, real-time GEX overlay, and weekly coaching. Or go all-in with Navigator for daily direct coaching with Ernie. Compare all plans here.