A debit spread is the simplest defined-risk structure in options trading — and the foundation that every advanced strategy builds on. You pay a debit at entry. Your maximum loss is that debit. Your maximum gain is the width of the spread minus what you paid. No margin calls. No unlimited exposure. No surprises. This is where structural options trading begins.

Most traders learn about this structure as a textbook concept and then skip ahead to more complex strategies. That is a mistake. The debit spread is not a stepping stone — it is the structural principle that makes butterfly spreads, iron butterflies, and every other defined-risk structure possible. Understanding how it works — mechanically, not theoretically — is what separates traders who manage risk from traders who hope for the best.

This guide covers both the call debit spread and the put debit spread, explains the critical debit spread vs credit spread comparison, and shows how structural 0DTE traders on SPX use this structure as the building block for asymmetric trades.

What Is a Debit Spread?

A debit spread is a two-leg options position where you buy one option and sell another at a different strike, both with the same expiration. The option you buy costs more than the option you sell, so the trade requires a net payment — the debit. That debit is your maximum risk.

The two main types are the call debit spread (bullish) and the put debit spread (bearish). Both follow the same logic: buy the option closer to the money and sell the option further from the money. The long option provides directional exposure. The short option reduces cost and caps your maximum gain at the width of the spread.

Every debit spread has three defined values at entry: the maximum loss (debit paid), the maximum gain (spread width minus debit), and the breakeven point (long strike plus or minus the debit). Nothing changes after entry except the probability of reaching each outcome. This is what makes it the cleanest risk structure available.

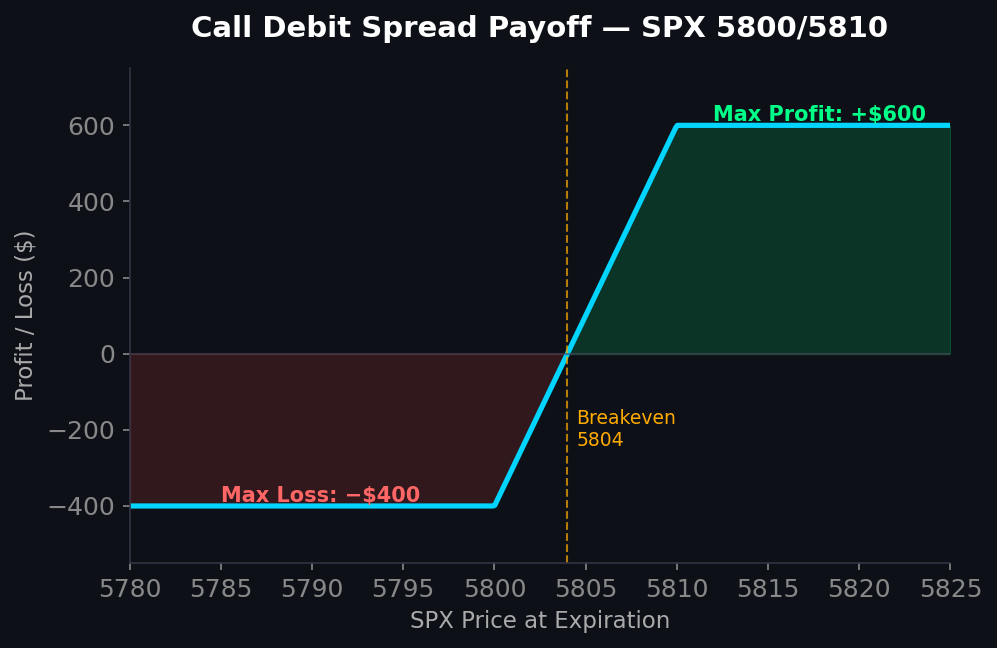

How a Call Debit Spread Works on SPX

A call debit spread profits when the underlying moves higher. The construction is straightforward:

- Buy one call at a lower strike (closer to or at the money)

- Sell one call at a higher strike (further out of the money)

Both options share the same expiration date and are traded on the same SPX options chain. The long call costs more than the short call, creating a net debit.

A concrete example on SPX at 5800: buy the 5800 call for $8.50 and sell the 5810 call for $4.50. The net debit is $4.00 ($400 per contract). Maximum profit is $10.00 minus $4.00 = $6.00 ($600 per contract) — achieved if SPX closes above 5810. Maximum loss is the $4.00 debit ($400) — and that only occurs if SPX closes below 5800. The breakeven is 5804.

The risk-to-reward ratio is $400 risk for $600 potential gain — 1.5:1 in your favor. Compare that to a naked long call at $8.50 ($850 risk) or a short strangle with undefined risk. The structure gives you directional exposure with a known worst case.

How a Put Debit Spread Works

A put debit spread profits when the underlying moves lower. The mirror image of the call version:

- Buy one put at a higher strike (closer to or at the money)

- Sell one put at a lower strike (further out of the money)

On SPX at 5800: buy the 5800 put for $8.00 and sell the 5790 put for $4.00. The net debit is $4.00. Maximum profit is $6.00 if SPX closes below 5790. Maximum loss is $4.00 if SPX closes above 5800. Breakeven is 5796.

This is the bearish counterpart. Same mechanics, same defined risk, opposite directional thesis. On 0DTE contracts, traders use the put version to express a bearish view after a structural breakdown — a failed test of resistance, a gamma flip, or a VIX spike mid-session.

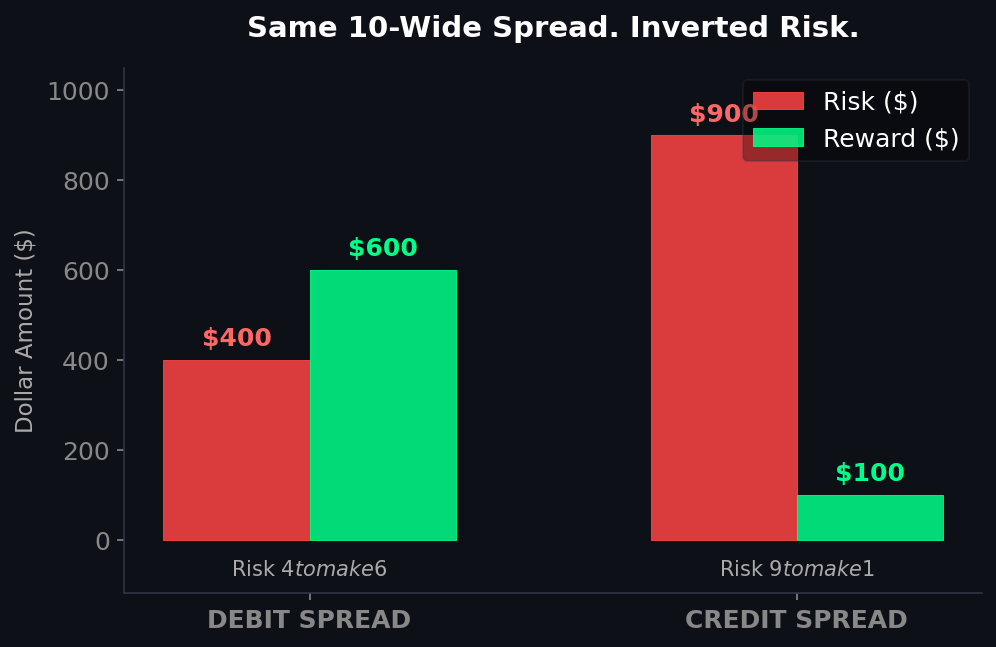

Debit Spread vs Credit Spread — The Risk Inversion

The debit spread vs credit spread comparison is the most important distinction in options strategy selection. They are structural inversions of each other.

A debit spread pays upfront and collects at expiration. You risk the debit for a larger potential gain. The trade starts at a loss and moves toward profit if the underlying cooperates. Maximum loss is known and paid at entry — it cannot grow.

A credit spread collects upfront and pays at expiration. You receive a credit and risk a larger potential loss. The trade starts at a profit and moves toward maximum loss if the underlying moves against you. Maximum loss is the spread width minus the credit — and on a 10-wide spread collecting $1.00, that means risking $9.00 to make $1.00.

The risk-to-reward profiles are inverted. A typical debit spread risks $4.00 to make $6.00. A typical credit spread of the same width collects $1.00 and risks $9.00. The credit spread wins more often — but when it loses, the loss is nine times the gain. Over hundreds of trades, this negative skew compounds. The debit structure wins less often but keeps losses small and gains larger. This is positive skew — and it is the foundation of every structural trading approach.

On 0DTE, the debit spread advantage is amplified. Gamma acceleration on expiration day means credit spreads can go from profitable to maximum loss in minutes. A 15-point SPX move through the short strike of a credit spread produces a loss that dwarfs the premium collected. The defined-risk position cannot lose more than what was paid — gamma works in your favor, not against you.

Why the Butterfly Is Two Vertical Spreads Combined

This is where the debit spread becomes the foundation for advanced structural trading.

A butterfly spread is constructed from two debit spreads sharing a common short strike — the body. A call butterfly at 5800 with 10-wide wings is:

- Call debit spread #1: Buy the 5790 call, sell the 5800 call

- Spread #2: Buy the 5810 call, sell the 5800 call (inverted — this is the bearish wing)

The result is a defined-risk structure that costs $0.40 to $1.50 and can return $8.50 to $9.60 if SPX settles at the 5800 body. The maximum loss is the tiny debit paid. The maximum gain is 5x to 25x the risk. This asymmetry — small defined loss, large potential gain — is only possible because each wing of the butterfly is a vertical spread with its own defined risk.

Understanding debit spread mechanics is what makes butterfly construction intuitive rather than mysterious. The butterfly is not a complex strategy. It is two simple vertical spreads pointed at the same target.

Width Selection and Timing on 0DTE

Width, strike selection, and timing determine whether a debit spread produces edge or bleeds premium.

Width follows VIX regime. In Zombieland (VIX below 17), use 5 to 10-wide spreads. The compressed range means narrower structures capture the move without overpaying. In Goldilocks (VIX 17 to 24), 10 to 15-wide spreads give room for larger intraday swings. Above VIX 24, the cost increases and the structure requires a larger move to profit — consider whether the setup justifies the wider structure.

Strike selection determines your probability. An at-the-money debit spread costs roughly 40% to 50% of the spread width — balanced risk and reward. A slightly out-of-the-money position costs 20% to 35% — cheaper entry but requires more movement. Deep OTM spreads cost under 15% but rarely reach maximum profit. For SPX 0DTE, slightly OTM structures offer the best structural edge.

Timing matters on expiration day. A debit spread entered at 9:45 AM has six hours of potential movement. The same position entered at 2:00 PM has 90 minutes — theta has already eroded much of the option value, so the debit is smaller but the window for the trade to work is compressed. Morning entries give more time. Afternoon entries give cheaper structures but demand faster directional confirmation.

Frequently Asked Questions

What is a debit spread in options?

A debit spread is a two-leg options strategy where you buy one option and sell another at a different strike, paying a net debit at entry. The debit paid is your maximum risk. The maximum gain is the spread width minus the debit. Both call debit spreads (bullish) and put debit spreads (bearish) follow this structure. It is the simplest defined-risk options position available.

What is the difference between a debit spread and a credit spread?

A debit spread pays upfront and profits if the underlying moves in your direction — risking $4 to make $6 on a typical setup. A credit spread collects premium upfront and profits if the underlying stays away from the short strike — collecting $1 and risking $9. The risk-to-reward profiles are inverted. Debit spreads have positive skew (small losses, larger gains). Credit spreads have negative skew (small gains, larger losses).

Is a call debit spread bullish or bearish?

A call debit spread is bullish. You buy a lower-strike call and sell a higher-strike call, profiting when the underlying moves above the upper strike by expiration. The put debit spread is the bearish counterpart — buy a higher-strike put and sell a lower-strike put, profiting when the underlying falls below the lower strike.

How much can you lose on a debit spread?

The maximum loss on a debit spread is exactly the debit paid at entry — nothing more. If you pay $4.00 for a 10-wide call debit spread, your maximum loss is $400 per contract regardless of how far the underlying moves against you. This defined-risk characteristic is what makes the structure the foundation for butterfly spreads and other asymmetric strategies.

Are debit spreads good for 0DTE trading?

Debit spreads are well-suited for 0DTE because the maximum risk is defined at entry and cannot expand — unlike credit spreads where gamma acceleration on expiration day can drive losses far beyond the credit collected. The debit is typically small on 0DTE contracts, keeping risk per trade low. Combining two of these spreads into a butterfly creates the asymmetric payoff structure that most 0DTE traders use.

Build From the Foundation

The debit spread is not glamorous. It does not promise 10x returns on a single trade or generate excitement in a Discord chat. What it does is define your risk at entry, cap your maximum loss at the debit paid, and create the structural foundation for every advanced options strategy worth trading.

At Fly on the Wall, every structure starts here. The butterfly is two vertical spreads combined. The iron butterfly inverts the debit into a credit with the same payoff. The width follows the VIX regime. The placement follows the expected move and GEX positioning. The structure follows the environment.

Start with the Observer for daily structural analysis and the tools that surface the expected move and market positioning before every session. Step up to Activator for full execution tools, real-time GEX overlay, and weekly coaching. Or go all-in with Navigator for daily direct coaching with Ernie. Compare all plans here.