A straddle option strategy is one of the purest volatility bets you can make. You’re not predicting direction — you’re predicting that the underlying will move, and move big enough to justify the premium you paid. It’s a simple structure with powerful implications, and understanding when it works (and when it doesn’t) separates informed traders from expensive gamblers.

The straddle is built from two options: a call and a put, both at the same strike price, both with the same expiration. That’s it. No complex multi-leg construction, no wing selection, no width decisions. Just one question: will the underlying move far enough from this strike to cover the cost of both options?

This guide covers the mechanics, math, and practical application of the straddle option strategy — including when to use it, when to avoid it, and how it fits into a broader options risk management framework.

How the Straddle Option Strategy Works

A long straddle involves buying both an at-the-money (ATM) call and an ATM put — a structure widely recognized as with the same strike and expiration. Your total cost is the combined premium of both options — and that’s also your maximum loss. The trade profits when the underlying moves significantly in either direction.

Long straddle construction:

- Buy 1 ATM call

- Buy 1 ATM put

- Same strike price

- Same expiration date

- Maximum loss = total premium paid (call premium + put premium)

- Breakeven points = strike price ± total premium paid

- Maximum profit = theoretically unlimited (upside) or substantial (downside, to zero)

For example, if SPX is trading at 5800, you might buy the 5800 call for $15.00 and the 5800 put for $14.50, paying a total of $29.50 ($2,950 per contract). Your breakeven points are 5770.50 on the downside and 5829.50 on the upside. SPX needs to move roughly 30 points in either direction for you to start profiting.

The Greeks Profile of a Straddle

Understanding the Greeks of a straddle tells you exactly what risks you’re taking and what market conditions favor the trade:

Delta: Near zero at initiation. The long call has positive delta and the long put has negative delta — they roughly cancel out. This is why a straddle is considered “delta neutral.” However, as the underlying moves, delta shifts quickly. Move up and your position becomes increasingly long delta. Move down and it becomes short delta. This is the feature, not a bug — the straddle is designed to accumulate directional exposure as the move develops.

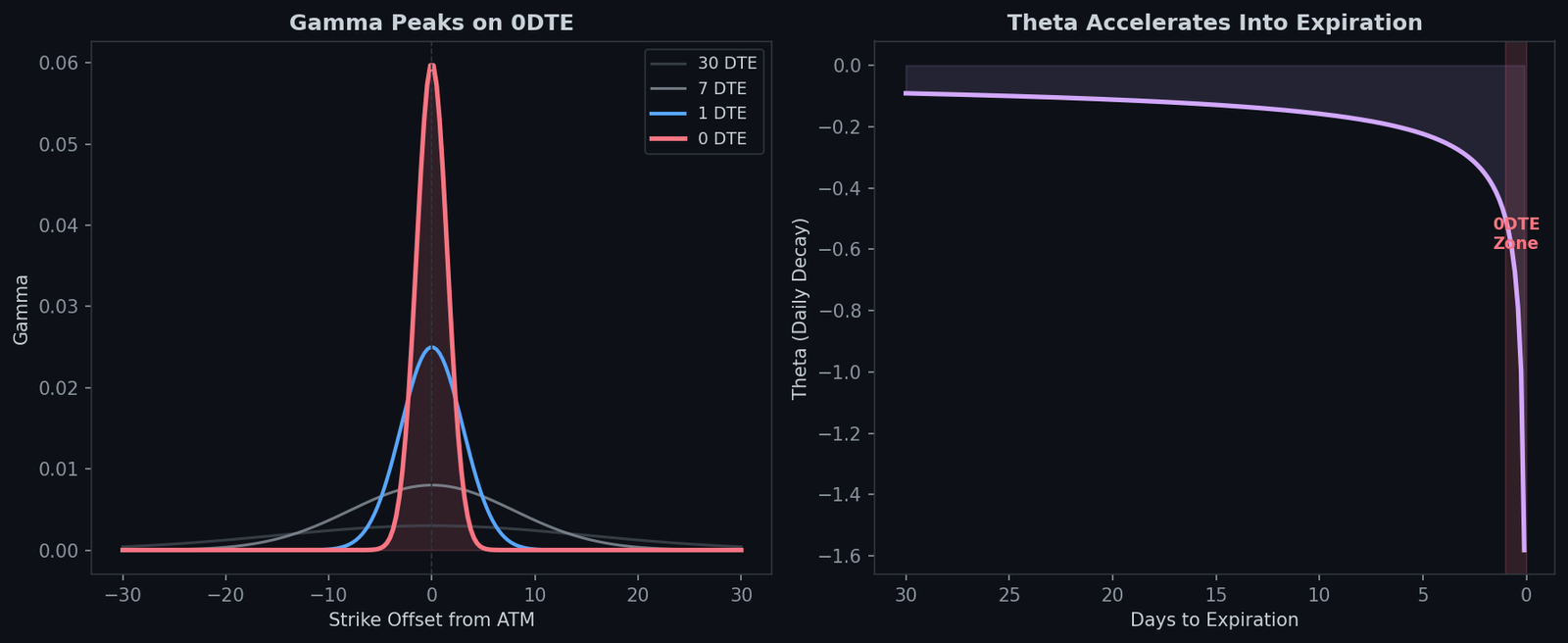

Gamma: High and positive. This is the engine of the straddle. High gamma means your delta changes rapidly with price movement, which is exactly what you want. ATM options have the highest gamma, so a straddle at the money gives you maximum gamma exposure. For 0DTE options, gamma is at its absolute peak — small moves create large delta shifts.

Theta: Negative and significant. This is the cost of the straddle. You’re paying time decay on two options simultaneously. Every day that passes without sufficient movement erodes your position. ATM options have the highest theta, meaning straddles bleed the fastest of any options structure. This creates a race between gamma (your friend) and theta (your enemy).

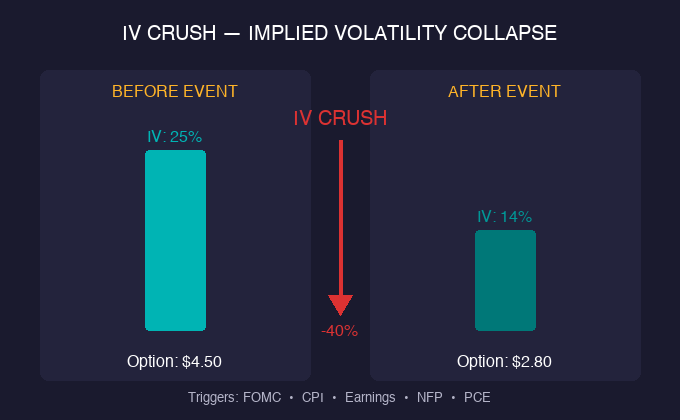

Vega: High and positive. A straddle benefits from rising implied volatility and suffers from falling IV. This makes entry timing critical — buying a straddle when IV is already elevated means you’re paying inflated premiums and exposed to IV crush if volatility contracts.

Long Straddle vs Short Straddle

Everything about the straddle flips when you sell instead of buy:

Long Straddle (Buying)

- Thesis: “I expect a big move but don’t know the direction”

- Max loss: Total premium paid (defined risk)

- Max profit: Unlimited (upside) / substantial (downside)

- Theta: Working against you

- Vega: Positive — benefits from IV expansion

- Best environment: Low IV before an expected catalyst, anticipated gamma squeeze

Short Straddle (Selling)

- Thesis: “I expect the underlying to stay near this price”

- Max loss: Unlimited (undefined risk)

- Max profit: Total premium received

- Theta: Working in your favor

- Vega: Negative — benefits from IV contraction

- Best environment: High IV that you expect to contract, range-bound market

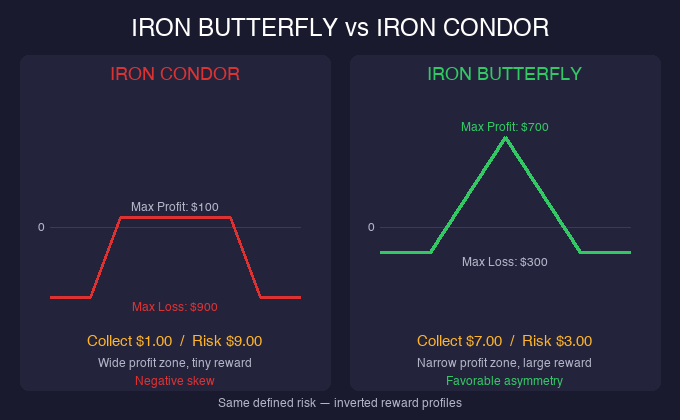

Short straddles carry substantially more risk. A single large move can produce losses that dwarf the premium collected. This is why short straddles require significantly more capital, strict risk management, and predefined exit rules. Most retail traders should focus on long straddles or consider defined-risk alternatives like iron butterflies if they want short volatility exposure.

When to Use a Straddle Option Strategy

Straddles work best in specific market conditions. Using one at the wrong time is the primary reason traders lose money with this structure.

Ideal Conditions for a Long Straddle

Before known catalysts with compressed IV. If a major event is approaching — earnings, FOMC, CPI release — and implied volatility hasn’t yet expanded to price in the expected move, a long straddle can capture the IV expansion itself plus the subsequent directional move. The key is getting in before the crowd, when options are still relatively cheap.

When the expected move seems too small. The options market prices in a statistical expected move for every expiration. If you believe the actual move will significantly exceed the expected move — because of a catalyst the market is underpricing or a structural dislocation — a straddle captures that excess movement.

Breakout setups from tight consolidation. When an underlying has been compressing into an increasingly tight range, a breakout in either direction is building. Long straddles positioned before the breakout benefit from the expansion, and the compressed IV during consolidation means cheaper entry prices.

When to Avoid Straddles

After IV has already expanded. Buying a straddle when IV is elevated means you’re paying inflated premiums. Even if the underlying moves, IV crush after the event can offset your directional gains. This is the classic “bought the straddle before earnings, stock moved 5%, and I still lost money” scenario.

In low-volatility, mean-reverting environments. If the market is in a structural low-volatility regime (VIX below 15, narrow daily ranges), straddles will bleed theta daily with insufficient movement to compensate. The gamma exposure profile favors mean reversion in these environments — working against long straddle holders.

With insufficient time. A 0DTE straddle is almost pure gamma — it either works immediately or theta destroys it by close. Longer-dated straddles give the thesis more time to play out but cost more in total premium. Match your timeframe to the catalyst you’re trading.

Straddle Option Strategy: Entry and Exit Rules

Having a systematic approach to straddle trading prevents emotional decision-making. Here’s a practical framework:

Entry Checklist

- Identify the catalyst: What event or condition do you expect to drive movement? No catalyst = no straddle.

- Check IV rank: Is current IV low relative to its range? Ideal entry is when IV rank is below 30 (options are cheap relative to recent history).

- Calculate the breakeven move: Total premium / underlying price = required percentage move. If this exceeds the historical average move for similar events, the straddle is overpriced.

- Size the position: Maximum loss = total premium paid. This should be 1-3% of your account per your risk management rules.

Exit Rules

- Profit target: Close at 50-100% of premium paid. A straddle that doubles means you’ve made 100% on your risk — take it.

- Time stop: If the catalyst has passed and the move hasn’t materialized, close immediately. Don’t hold a straddle hoping for a delayed reaction.

- Loss limit: Close if the position has lost 50% of its value. This typically means the underlying stayed range-bound and theta has eaten half your premium.

- Leg management: If the underlying has moved significantly in one direction, consider closing the profitable leg and letting the losing leg ride as a cheap lottery ticket — but only if you’ve already locked in profit on the winning side.

Straddle vs Other Volatility Strategies

The straddle isn’t the only way to express a volatility view. Understanding the alternatives helps you choose the right structure for each situation:

Straddle vs Strangle: A strangle uses different strikes (OTM call + OTM put) making it cheaper but requiring a larger move to profit. Straddles have higher gamma but higher cost. Strangles are the budget version with wider breakevens. For a detailed comparison, see our straddle vs strangle guide.

Straddle vs Butterfly: A butterfly is a directional or pinning bet with defined risk and lower cost, but it requires precision on direction and timing. Straddles sacrifice the asymmetric payoff for the freedom of not needing to pick direction.

Straddle vs Iron Butterfly: An iron butterfly is essentially a short straddle with protective wings. It defines the risk that a naked short straddle leaves undefined, making it a more practical short-volatility alternative for most traders.

Straddle vs Debit Spread: Debit spreads are directional with defined risk and lower cost, but require you to correctly predict direction. Straddles pay more but remove the directional requirement. If you have a directional view, a debit spread is more capital-efficient. If you don’t, the straddle is the honest structure.

Straddle Option Strategy Mistakes to Avoid

Buying straddles habitually before every event. Not every catalyst produces a move that exceeds the straddle cost. If implied volatility has already expanded to price in the event, the options market is telling you the move is already expected. You need to believe the actual move will exceed the priced-in expected move — and have a reason for that belief beyond “big events cause big moves.”

Ignoring the total cost of the trade. A straddle on SPX might cost $30+ (that’s $3,000+ per contract). This isn’t an inexpensive trade, and the full premium is at risk. Always calculate your maximum loss in dollar terms, not just as a percentage of the underlying’s price.

Holding through IV crush. If you bought a straddle before an event, the moment the event passes, IV collapses. Even if the underlying moved in your favor, the vega loss from IV crush can offset the gamma gains from the move. Set a time-based exit at or immediately after the catalyst.

Selling straddles without defined stops. Short straddles have unlimited risk. A gamma squeeze or gap move can produce losses of 5-10x the premium received. Always have a predefined exit point, and consider using an iron butterfly instead for defined-risk short volatility exposure.

Using straddles as a crutch for indecision. “I don’t know which way it’s going, so I’ll buy both” is not a strategy — it’s an admission that you haven’t done the work. A straddle should be a deliberate volatility trade, not a way to avoid forming a directional view. If you don’t have a volatility thesis, you don’t have a trade.

Frequently Asked Questions

What is a straddle option strategy?

A straddle option strategy involves simultaneously buying (or selling) a call and a put at the same strike price and expiration date. A long straddle profits from large price movement in either direction, while a short straddle profits when the underlying stays near the strike price. Your maximum loss on a long straddle is the total premium paid for both options.

When should you buy a straddle option?

Buy a straddle when you expect a significant price move but are uncertain about the direction. The ideal setup is before a known catalyst (earnings, economic data, FOMC) when implied volatility is still low relative to its recent range. Avoid buying straddles after IV has already expanded, as IV crush after the event can offset directional gains.

How much can you lose on a straddle?

On a long straddle, your maximum loss is the total premium paid for the call and put combined. For example, if you pay $15 for the call and $14 for the put, your max loss is $29 per share ($2,900 per contract on SPX). On a short straddle, losses are theoretically unlimited on the upside and substantial on the downside, which is why short straddles require strict risk management.

Is a straddle better than a strangle?

Neither is inherently better — they serve different purposes. Straddles cost more but have tighter breakevens and higher gamma, meaning they profit faster from movement. Strangles cost less but require a larger move to reach profitability. If you expect a moderate move, the strangle’s lower cost is advantageous. If you expect an explosive move, the straddle’s higher gamma captures more profit.

Can you make money selling straddles?

Yes, but with significant risk. Short straddle sellers profit when the underlying stays near the strike price and time decay erodes both options. The strategy works best when implied volatility is elevated and expected to contract. However, short straddles carry unlimited risk, and a single large move can produce catastrophic losses. Most traders who sell straddles use iron butterflies instead to cap their maximum loss while maintaining a similar profit profile near the strike.