A credit spread is the most popular options strategy for traders who want to collect premium with defined risk. You sell an option, buy a cheaper option further out of the money as protection, and pocket the difference. The credit hits your account immediately. The trade wins if price stays away from your short strike. Simple, high win rate, and — for most traders — quietly destructive over time.

The credit spread is not a bad strategy. It is a misunderstood one. The structure works exactly as designed — it just designs for a risk profile that most traders do not recognize until they have lived through enough losing months to see the pattern. This guide explains what a credit spread is, how it works on SPX, why the math favors the house over hundreds of trades, and what structural alternatives exist for traders who want defined risk without negative skew.

What Is a Credit Spread in Options?

A credit spread is a two-leg options position where you sell one option and buy another at a further strike, both with the same expiration. The option you sell is worth more than the option you buy, so the trade generates a net credit — cash received at entry.

The two main types are the bull put credit spread (bullish — sell a put, buy a lower put) and the bear call credit spread (bearish — sell a call, buy a higher call). Both follow the same logic: collect premium by selling the closer-to-the-money option and limit your maximum loss by buying protection further out.

The maximum profit is the credit received. The maximum loss is the width of the spread minus the credit. The breakeven is the short strike minus the credit received (for put spreads) or plus the credit received (for call spreads).

How a Bull Put Credit Spread Works on SPX

The bull put spread is the most common credit spread — a bullish bet that collects premium if price stays above the short strike.

- Sell one put at a higher strike (closer to the money)

- Buy one put at a lower strike (further out of the money)

On SPX at 5800: sell the 5790 put for $4.50 and buy the 5780 put for $1.50. The net credit is $3.00 ($300 per contract). Maximum profit is $300 if SPX closes above 5790 at expiration — you keep the entire credit. Maximum loss is $10.00 minus $3.00 = $7.00 ($700 per contract) if SPX closes below 5780.

The win rate on this trade is high. SPX only needs to stay above 5790 — a level already 10 points below the current price. In a range-bound session, this happens often. The problem is not the individual trade. The problem is what happens over 100 of them.

The Math That Hides Behind High Win Rates

This is where the credit spread reveals its true risk profile.

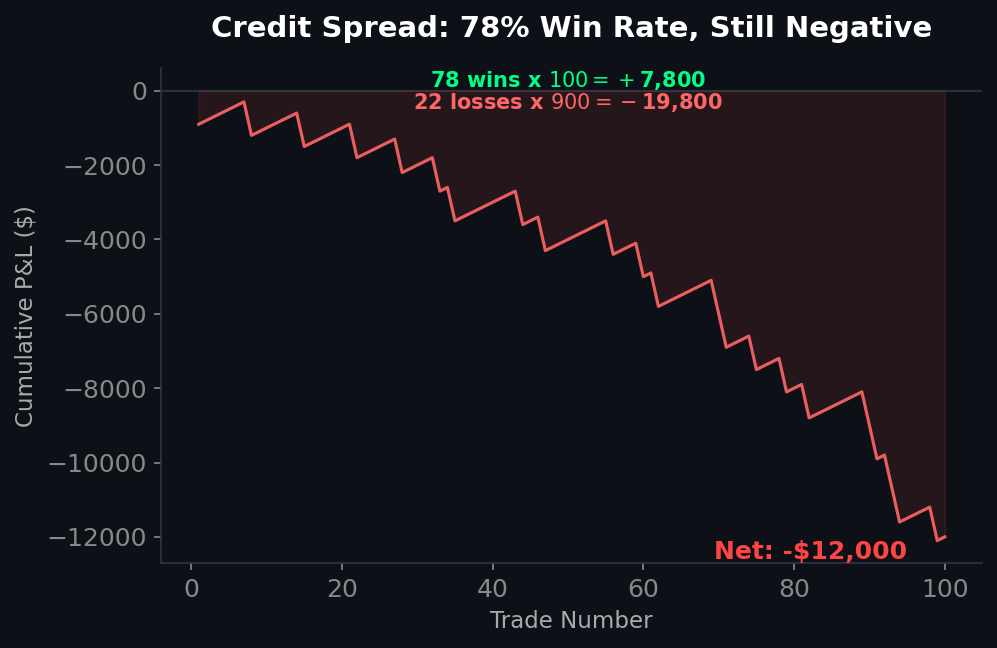

A typical credit spread collects $1.00 and risks $9.00 on a 10-wide spread. The win rate might be 75% to 85% — you keep the $100 credit on most trades. But when the trade loses, it loses $900. One loss erases nine wins. Over 100 trades at a 78% win rate, you collect $7,800 in winners and lose $19,800 in losers. Net result: negative $12,000.

The numbers improve slightly with wider credits. A spread collecting $3.00 and risking $7.00 has better math — but the win rate drops because the short strike is closer to the money. The fundamental relationship holds: credit spreads produce negatively skewed return distributions. Small frequent wins. Large occasional losses. The wins feel good. The losses compound.

This is not a theoretical problem. Every experienced premium seller has lived through the month where one or two trades erase three months of carefully collected premium. The drawdown is not a surprise — it is the structure working exactly as the math predicts. The credit spread does not have a flaw. It has a feature that most traders mistake for edge.

Credit Spread vs Debit Spread — The Structural Inversion

The credit spread and the debit spread are mirror images. Understanding the difference is the first step toward recognizing which risk profile you are actually trading.

The credit spread collects at entry and pays at expiration. You receive $1.00 and risk $9.00. The trade starts profitable and deteriorates if the underlying moves against you. You are selling probability — collecting small premiums in exchange for bearing the tail risk of a large loss.

The debit spread pays at entry and collects at expiration. You risk $4.00 and can make $6.00. The trade starts at a loss and profits if the underlying moves in your direction. You are buying asymmetry — paying a small premium for the chance at a larger gain.

The skew profiles are inverted. Credit spreads produce negative skew: most outcomes are small gains, a few outcomes are large losses. Debit spreads produce positive skew: most outcomes are small losses, a few outcomes are larger gains. Over hundreds of trades, positive skew compounds in your favor. Negative skew compounds against you — even when the win rate is high.

On 0DTE contracts, the inversion is amplified. Gamma acceleration on expiration day means a credit spread can move from profitable to maximum loss in minutes. A 20-point SPX move through the short strike produces a loss that no amount of theta collection can recover within the session. The debit spread caps your loss at the debit paid regardless of how far or fast price moves.

Why Credit Spreads Fail Around Events

The worst sessions for premium sellers are the sessions with the largest moves — and those sessions are predictable.

Economic releases create the exact conditions that destroy credit spreads. Before CPI, FOMC, or NFP, implied volatility is elevated. This makes the credit collected on a spread appear larger than normal, which attracts sellers. Then the number prints, the market moves 30 to 50 points in a direction, and every credit spread on the wrong side hits maximum loss in minutes. The IV crush that follows cannot help — the directional damage is already done.

Trending sessions are equally destructive. A credit spread sold at the open on a day that trends 60 points in one direction will reach maximum loss with no opportunity to manage. The high win rate on range-bound days creates false confidence that gets destroyed on the trending days that define your actual return distribution.

The correlation is structural. The sessions that produce the largest losses are the same sessions where implied volatility was elevated — which means the credit collected was at its highest. Traders sell the most premium precisely when the risk of a large adverse move is greatest. This is not bad luck. It is the mechanics of the strategy working against you.

What Structural Traders Use Instead

The convergence thesis behind a credit spread — price stays near a level and you profit from that stillness — is not wrong. The problem is the vehicle, not the thesis.

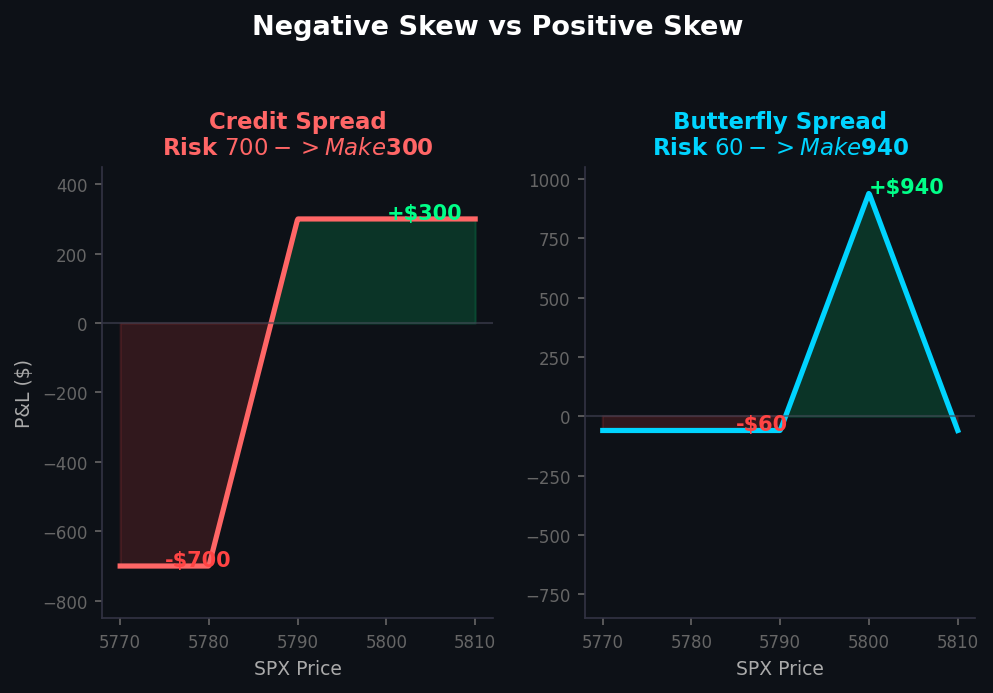

The iron butterfly captures the same convergence thesis with better math. Instead of selling a credit spread that risks $9 to make $1, the iron butterfly sells a straddle at the body and buys protective wings. The result: collect $7 and risk $3 on a 10-wide structure. Same defined risk. Same convergence play. Inverted reward-to-risk ratio.

The butterfly spread removes the premium-selling component entirely. A debit butterfly costs $0.40 to $1.50 and can return $8.50 to $9.60 if price settles at the body. Maximum loss is the debit paid. No short premium to defend. No gamma acceleration working against you. No IV crush erasing your edge. The butterfly achieves price convergence profits through a defined-risk debit structure — positive skew by design.

The iron condor is the credit spread’s natural evolution — but it shares the same flaw. An iron condor is two credit spreads combined (a bull put and a bear call). The profit zone is wider but the risk-to-reward ratio remains negatively skewed. It wins more often than a single credit spread, but the losses when they come are the same or larger. Structural traders who understand skew eventually move past the iron condor toward butterfly-based structures.

When a Credit Spread Actually Makes Sense

The credit spread is not always wrong. There are specific conditions where it earns its place.

As a hedge, not a primary strategy. A bear call credit spread sold above a strong resistance level — backed by GEX data showing negative gamma above that level — can protect a long portfolio against upside that is structurally unlikely. The credit received reduces the cost of the hedge.

As part of a larger structure. Every iron butterfly and iron condor contains credit spreads as components. The credit spread is not the problem — the naked credit spread as a standalone strategy is the problem. When embedded in a structure with defined maximum loss and favorable reward-to-risk, the credit spread component serves its purpose.

With strict position sizing. If the maximum loss on a credit spread represents less than 1% of the trading account, the negative skew becomes manageable. The issue arises when traders size based on the credit received rather than the maximum loss — collecting $100 per contract while risking $900 and running five contracts because the win rate feels safe.

Frequently Asked Questions

What is a credit spread in options?

A credit spread is a two-leg options strategy where you sell one option and buy a cheaper option further out of the money, collecting a net credit at entry. The maximum profit is the credit received. The maximum loss is the spread width minus the credit. Bull put spreads (bullish) and bear call spreads (bearish) are the two main types.

Why do credit spreads lose money over time?

Credit spreads produce negatively skewed returns — small frequent wins and large occasional losses. A typical 10-wide spread collects $1 and risks $9. Even with a 78% win rate, one loss erases nine wins. Over hundreds of trades, this negative skew compounds against you. The strategy works on any individual trade but the distribution of outcomes favors the losing side over time.

Are credit spreads good for beginners?

Credit spreads appeal to beginners because of the high win rate and immediate premium received. However, the risk profile is deceptive. New traders often size positions based on the credit collected rather than the maximum loss, which leads to outsized drawdowns when the inevitable losing trade occurs. Understanding the negative skew before trading credit spreads is essential.

What is the difference between a credit spread and an iron condor?

An iron condor is two credit spreads combined — a bull put spread below the current price and a bear call spread above. The iron condor has a wider profit zone and collects premium from both sides, but the risk-to-reward ratio remains negatively skewed. Both structures share the same fundamental limitation: small wins, large losses, and a return distribution that compounds against you.

What is a better alternative to credit spreads?

Butterfly spreads offer the same convergence thesis — profiting when price settles near a target level — but with positively skewed risk. A butterfly costs $0.40 to $1.50 and can return $8.50 to $9.60. Maximum loss is the small debit paid. No short premium exposure, no gamma acceleration against you, and no IV crush risk. The iron butterfly is another alternative that collects a credit but inverts the risk-to-reward ratio in your favor.

Understand the Structure Before You Sell It

The credit spread is not a scam and it is not broken. It does exactly what it is designed to do — collect premium in exchange for bearing tail risk. The question is whether that exchange favors you over hundreds of trades. For most traders selling standalone credit spreads on SPX, the answer is no.

At Fly on the Wall, the structural approach replaces the credit spread’s negative skew with the butterfly’s positive skew. The expected move defines the range. The GEX overlay shows where price is likely to pin. The VIX regime determines your width. And the butterfly captures the convergence thesis without the compounding losses that erode premium-selling accounts over time.

Start with the Observer for daily structural analysis and the tools that surface the expected move and market positioning before every session. Step up to Activator for full execution tools, real-time GEX overlay, and weekly coaching. Or go all-in with Navigator for daily direct coaching with Ernie. Compare all plans here.