The options Greeks are the five variables that determine how an option’s price changes in response to market conditions. Delta, gamma, theta, vega, and rho. Every options strategy — every spread, every butterfly, every iron condor — is a combination of Greek exposures. Understanding the options Greeks is not about memorizing formulas. It is about knowing which forces are acting on your position and whether those forces are working for you or against you.

Most traders learn the Greeks as isolated definitions and then struggle to connect them to actual trading decisions. That is because the Greeks do not exist in isolation. They interact. Gamma amplifies delta. Theta accelerates near expiration. Vega collapses after events. On 0DTE contracts, these interactions are compressed into hours instead of weeks — which means understanding the Greeks is not academic. It is the difference between a structure that works and one that decays before it has a chance.

This guide explains each of the options Greeks in practical terms, shows how they interact on SPX, and identifies which Greeks matter most for structural 0DTE trading.

Delta — Directional Exposure

Delta measures how much an option’s price changes for every one-point move in the underlying. A call with a delta of 0.50 gains $0.50 when SPX moves up one point. A put with a delta of -0.40 gains $0.40 when SPX moves down one point.

Delta tells you the directional bias of your position. A long call has positive delta — it profits from upward movement. A long put has negative delta — it profits from downward movement. A butterfly centered at the current price has near-zero delta at entry — it is direction-neutral and profits from price convergence rather than direction.

Delta changes as price moves. An at-the-money option has a delta near 0.50. As the option moves deeper in the money, delta approaches 1.00. As it moves further out of the money, delta approaches 0. This is not a static number — it shifts with every tick of the underlying. The rate of that shift is gamma.

Among the options Greeks, delta determines placement for 0DTE traders. A butterfly placed with the body at the money starts delta-neutral. A butterfly placed five points above the current price has positive delta — a directional bet that price will rise to the body. Strike selection is delta selection.

Gamma — The Options Greek That Dominates 0DTE

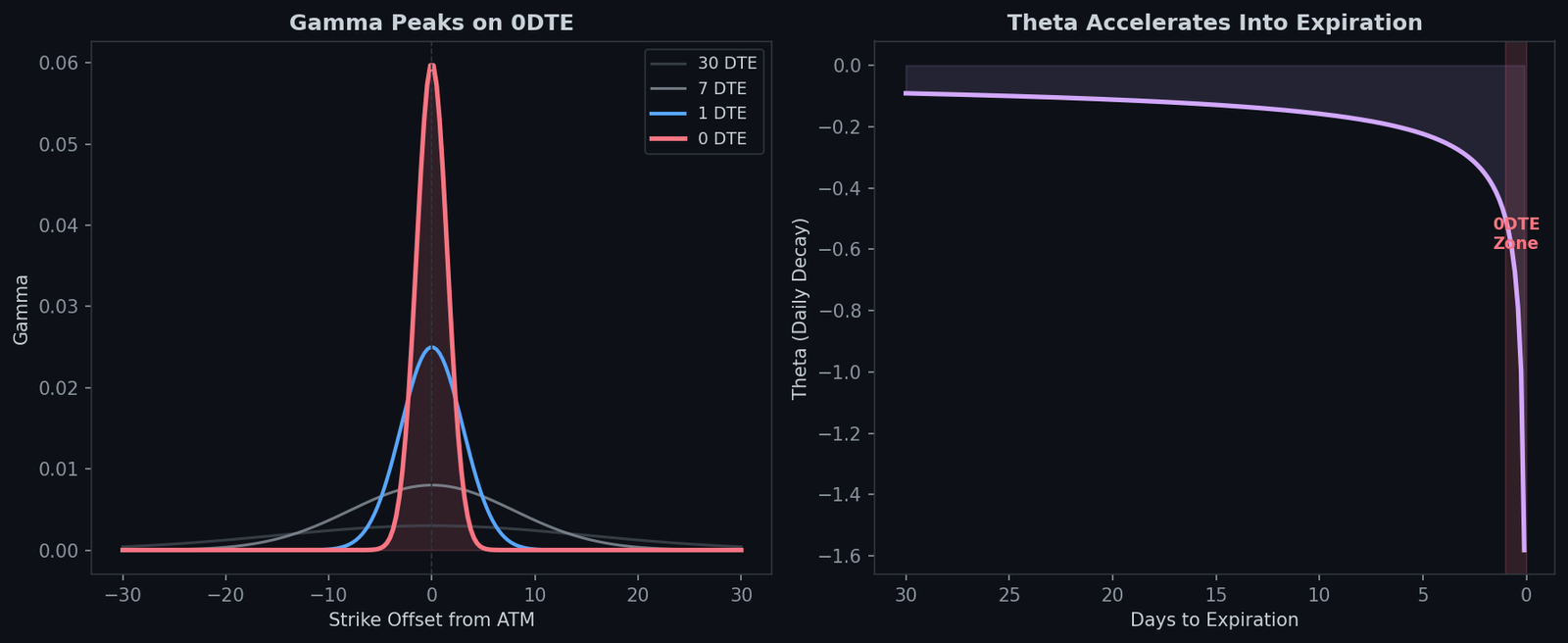

Of all the options Greeks, gamma is the one that defines 0DTE risk. Gamma measures the rate of change of delta. If delta tells you your current speed, gamma tells you your acceleration. A high gamma position sees its delta change rapidly with every point of movement. A low gamma position is more stable.

Gamma is highest at the money and near expiration. This is the single most important fact for 0DTE traders. On the last day of an option’s life, at-the-money options have explosive gamma. A one-point SPX move changes delta dramatically, which means the P&L acceleration on 0DTE contracts is unlike any other timeframe.

Gamma is the friend of buyers and the enemy of sellers. If you own options (long gamma), price movement generates profit that accelerates — each additional point of movement is worth more than the last. If you have sold options (short gamma), price movement generates losses that accelerate. This is why credit spreads and short strangles can move from profitable to maximum loss in minutes on 0DTE.

Gamma exposure (GEX) at the market level determines whether dealers are amplifying or dampening price movement. Positive GEX means dealers hedge in a way that stabilizes price. Negative GEX means dealer hedging amplifies directional moves. Understanding gamma at both the position level and the market level is what separates structural traders from directional gamblers.

Theta — Time Decay

Theta measures the daily erosion of an option’s time value. An option with a theta of -$0.50 loses $0.50 of value every day, all else equal. Theta is always negative for option buyers and positive for option sellers.

Theta accelerates into expiration. An option loses more value in its final week than in any prior week. On the final day — 0DTE — theta decay is at its most aggressive. An at-the-money SPX option might lose 30% to 50% of its remaining value in the last two hours of trading. This acceleration is what makes 0DTE trading fundamentally different from weekly or monthly strategies.

Theta benefits butterfly traders in a specific way. A butterfly spread is long two outer wings and short two at-the-money options. The short options at the body decay faster than the long wings because at-the-money options have the highest theta. As expiration approaches, the body decays toward zero faster than the wings — which is exactly how the butterfly reaches its maximum value. Theta is actively working to push the butterfly toward its payoff.

In the options Greeks framework, theta is the attraction for premium sellers and gamma is the trap. Theta puts money in your account every day. But gamma can take it all back in an hour. The iron butterfly resolves this conflict by collecting theta at the body while capping the gamma risk with protective wings. The naked short straddle collects the same theta but has unlimited gamma exposure.

Vega — Volatility Sensitivity

Vega measures how much an option’s price changes for every one-percentage-point change in implied volatility. An option with a vega of $0.15 gains $0.15 if implied volatility rises by one point and loses $0.15 if it falls by one point.

Vega is highest on longer-dated options and lowest on 0DTE. This is critical. With hours until expiration, implied volatility changes have minimal impact on option prices because there is almost no time left for that volatility to manifest. On 0DTE contracts, gamma and theta dominate while vega is nearly irrelevant. This is why IV crush — the collapse of implied volatility after an event — devastates monthly option sellers but barely affects 0DTE butterfly traders.

Within the options Greeks, vega matters most before events on longer-dated contracts. If you hold a weekly straddle through an FOMC decision, the IV crush after the announcement can destroy your position even if the directional move was in your favor. The vega component collapses and takes the option’s value with it. This is a vega problem, not a delta problem.

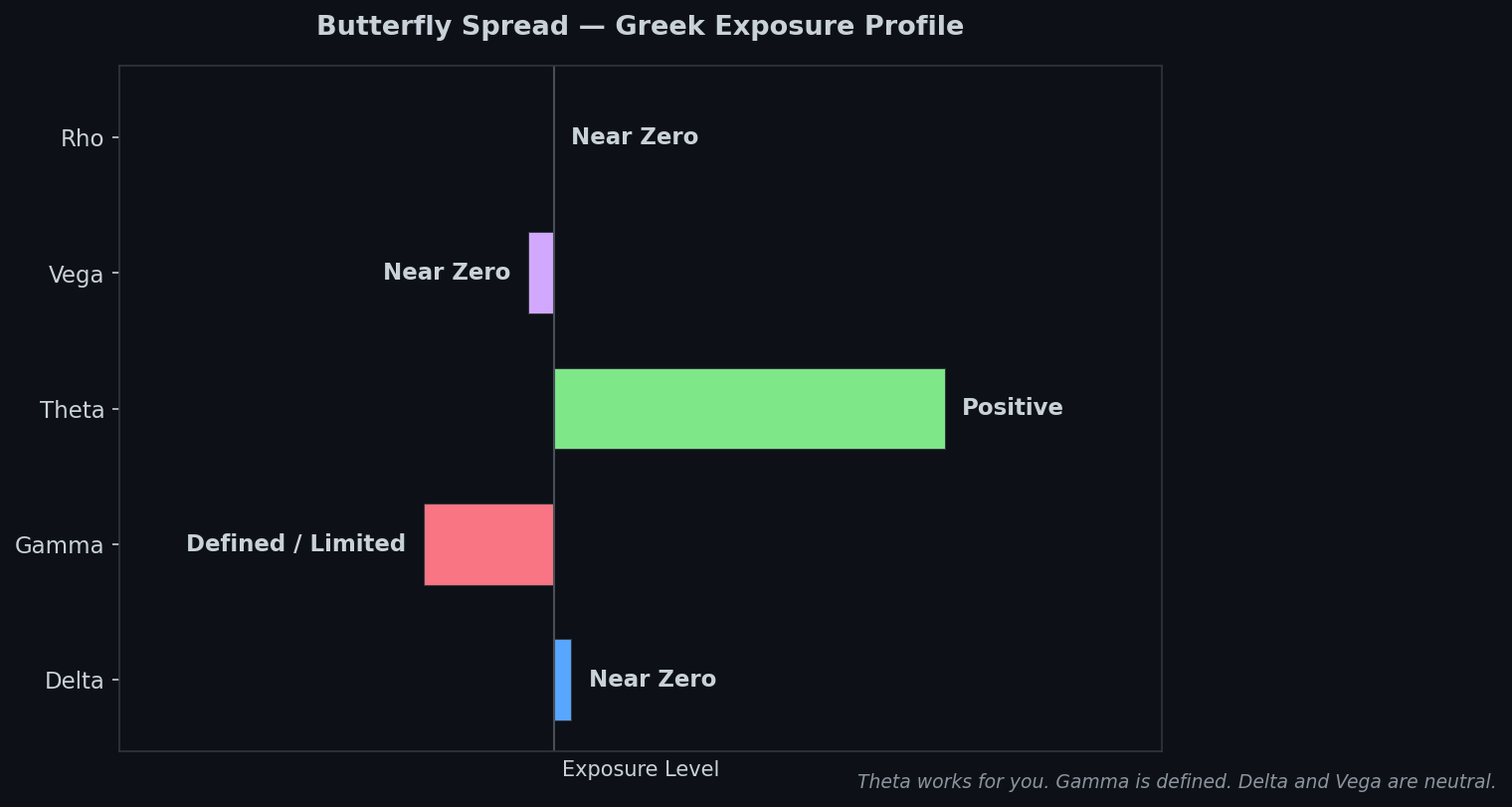

Butterflies have near-zero net vega. Because the long wings and short body partially offset each other’s vega exposure, the butterfly is largely insensitive to implied volatility changes. This structural vega neutrality is one reason the butterfly is the preferred 0DTE structure — it eliminates an entire Greek from the risk equation.

Rho — The Greek That Rarely Matters

Rho measures sensitivity to interest rate changes. In the options Greeks hierarchy, rho is the least relevant for most traders. Interest rate changes are gradual and priced in well before they affect option premiums. On 0DTE contracts, rho is functionally zero.

The only scenario where rho matters is on deep in-the-money LEAPS held for months or years, where the cost of carry becomes a meaningful component of the option’s value. For SPX intraday trading, rho can be safely ignored.

How the Options Greeks Interact on 0DTE

The options Greeks do not operate independently. On 0DTE contracts, their interactions create the distinctive dynamics that define same-day trading.

Gamma and theta are in constant tension. Theta puts money in the pocket of premium sellers every minute. But gamma takes it back with every point of adverse movement — and the magnitude of gamma’s bite increases as expiration approaches. A credit spread sold at 10:00 AM benefits from six hours of theta decay. But a 20-point adverse move at 2:00 PM — when gamma is at its peak — can erase all of that decay in minutes.

Delta becomes binary near expiration. An at-the-money option with two hours left has a delta near 0.50. With 15 minutes left, a one-point move in either direction can push delta to 0.80 or 0.20. The option either expires in the money or worthless — the delta is converging toward 1 or 0. This is why position management in the final hour requires rapid decision-making.

Vega fades to irrelevance. By the afternoon of expiration day, implied volatility changes barely move option prices. The expected move has either played out or it has not. Vega is no longer a factor in your P&L — only gamma and theta remain.

The butterfly exploits this interaction perfectly. It benefits from theta decay at the body. It has defined gamma risk through the long wings. It is vega-neutral. And its delta is managed through body placement relative to price. Every Greek is accounted for in the structure — no exposure is left unhedged.

Frequently Asked Questions

What are the options Greeks?

The options Greeks are five measurements that describe how an option’s price responds to changes in market conditions. Delta measures directional sensitivity, gamma measures the acceleration of delta, theta measures time decay, vega measures volatility sensitivity, and rho measures interest rate sensitivity. Together they define the complete risk profile of any options position.

Which Greek is most important for 0DTE trading?

Gamma is the dominant Greek on 0DTE. With hours until expiration, gamma is at its peak — meaning every point of price movement creates larger P&L swings than on any other timeframe. Theta is second, aggressively eroding time value throughout the session. Vega is nearly irrelevant on 0DTE because there is not enough time left for implied volatility changes to meaningfully affect prices.

How do the Greeks affect butterfly spreads?

Butterflies have a favorable Greek profile for 0DTE trading. They start near delta-neutral (direction-agnostic), benefit from theta decay at the body, have defined gamma risk through the protective wings, and are vega-neutral because the long and short legs offset each other. This means butterflies are primarily driven by price convergence and time decay rather than volatility changes.

What is the difference between delta and gamma?

Delta measures the current rate of price change — how much the option moves per point of underlying movement. Gamma measures how fast delta itself is changing. If delta is your speed, gamma is your acceleration. A high-gamma position sees rapid P&L acceleration as price moves, which is why gamma dominates the risk profile on 0DTE contracts where it peaks near expiration.

Why does theta accelerate near expiration?

Time value erodes faster as expiration approaches because there is less time for the option to become profitable. An option with 30 days left loses a small amount daily. The same option with one day left loses a large percentage of its remaining value in hours. On 0DTE, at-the-money options can lose 30% to 50% of their value in the final two hours — which is why theta decay is the primary driver of butterfly profitability on expiration day.

Trade the Options Greeks, Not Against Them

The options Greeks are not obstacles to navigate around. They are forces to align with. A well-constructed position puts gamma, theta, and delta on your side while neutralizing vega. A poorly constructed position fights one or more Greeks every minute of the session.

At Fly on the Wall, Greek alignment is built into every structure. The GEX overlay shows where gamma exposure at the market level supports your thesis. The expected move translates implied volatility into actionable price ranges. The VIX regime determines which structures have the right Greek exposure for the session. And the butterfly — with its defined gamma, favorable theta, neutral vega, and adjustable delta — is the structure that puts all five Greeks to work.

Start with the Observer for daily structural analysis and the tools that surface the expected move and market positioning before every session. Step up to Activator for full execution tools, real-time GEX overlay, and weekly coaching. Or go all-in with Navigator for daily direct coaching with Ernie. Compare all plans here.