Options market structure is the invisible machinery that determines how your orders get filled, why prices move the way they do, and who’s on the other side of every trade you take. Most traders focus entirely on strategy — which spread to trade, where to place strikes, how to manage Greeks — without understanding the structural forces that shape the environment they’re operating in. That’s like learning to sail without understanding tides and currents.

The options market is not a simple buyer-meets-seller marketplace. It’s a layered ecosystem of exchanges, market makers, dealers, clearing houses, and institutional participants, each with different incentives and behaviors. Understanding this structure gives you an edge that no technical indicator can replicate — because it tells you why prices move, not just that they moved.

This guide breaks down how the SPX options market actually works, from order execution to the dealer dynamics that drive intraday price action in 0DTE trading.

How Options Orders Get Executed

When you submit an order to buy a butterfly or sell a credit spread, the process is more complex than it appears on your broker’s confirmation screen.

The Exchange Layer

SPX options trade on the CBOE (Chicago Board Options Exchange), which is the primary and original listing exchange for S&P 500 index options. Unlike equity options that trade across 16+ exchanges, SPX options are exclusively listed on the CBOE. This concentration means all SPX liquidity flows through a single venue — which actually improves execution quality by preventing fragmentation.

The exchange operates an electronic order book where bids and offers are matched. However, most retail orders don’t interact directly with the central order book. Instead, they’re routed through a series of intermediaries.

Order Flow: From Your Click to the Fill

- Your broker receives your order and applies best execution obligations

- The order is routed — either directly to the exchange or to a market maker who provides price improvement

- On the exchange, your order enters an auction process where market makers compete to fill it

- The trade is matched and reported back to your broker

- The OCC (Options Clearing Corporation) steps in as the central counterparty — guaranteeing settlement on both sides

The entire process takes milliseconds. But within those milliseconds, multiple market makers are evaluating your order, calculating their risk, and deciding whether to fill it — and at what price. Understanding who these market makers are and how they behave is where the structural edge lies.

Market Makers: The Engine of Liquidity

Market makers are the most important participants in options market structure. They provide the liquidity that allows you to enter and exit positions. Without them, the bid-ask spread on your butterfly would be so wide that the trade wouldn’t be worth taking.

What Market Makers Actually Do

Market makers continuously post bids and offers across thousands of option strikes simultaneously. They profit from the bid-ask spread — buying at the bid and selling at the ask. But they’re not taking directional bets on the market. Their goal is to remain delta-neutral, collecting the spread while hedging away directional risk.

This hedging behavior is the key to understanding how options market structure drives price action. When a market maker sells you an SPX call, they immediately buy SPX futures or ETFs to hedge their delta exposure. When they sell you a put, they sell futures to hedge. This hedging activity creates mechanical flows in the underlying market that are predictable based on options positioning.

The Dealer Hedging Feedback Loop

This is where options market structure directly impacts your trading. When dealers are collectively “long gamma” (they’ve bought more options than they’ve sold), their hedging activity suppresses volatility. As SPX rises, they sell futures to rebalance. As SPX falls, they buy futures. This creates a dampening effect that compresses daily ranges.

When dealers are “short gamma” (they’ve sold more options than they’ve bought), the opposite happens. As SPX rises, they buy futures. As SPX falls, they sell futures. This amplifies volatility, creating larger moves and trending behavior. This is the structural foundation behind gamma exposure (GEX) analysis.

The practical implication: when GEX is positive (dealers long gamma), expect mean-reversion and narrower ranges. When GEX is negative (dealers short gamma), expect trend continuation and wider ranges. This isn’t a theory — it’s a direct consequence of how the hedging mechanics work within the options market structure.

Institutional Participants and Their Impact

Retail traders like you and me are a relatively small part of the SPX options market by volume. Understanding who the large participants are — and what they’re doing — provides critical context.

Institutional Hedgers

Pension funds, mutual funds, and insurance companies use SPX options to hedge their equity portfolios. Their primary activity is buying protective puts — which creates persistent demand for downside protection. This structural demand is why SPX put implied volatility is almost always higher than call IV (the “volatility skew”). It’s not because the market is always bearish — it’s because institutions are always hedging.

Volatility Funds

Dedicated volatility trading firms — systematic and discretionary — trade the VIX complex, variance swaps, and SPX options to express views on volatility itself. Their flows can amplify or dampen market moves depending on their positioning. When volatility funds are short vol (which is common in low-VIX environments), a sudden spike forces them to cover — adding fuel to sell-offs.

0DTE Retail Flow

The explosion of 0DTE options trading since 2022 has introduced a new structural force. Daily options volume now regularly exceeds $1 trillion in notional value. This concentrated short-dated flow creates massive gamma exposure at near-term strikes, which market makers must hedge in real time. The result: expiration day dynamics are more volatile and more structurally driven than ever.

The OCC: Counterparty Risk Elimination

The Options Clearing Corporation (OCC) is the central counterparty for all listed options in the United States. When you trade an SPX option, the OCC steps between you and the other side — guaranteeing that both parties fulfill their obligations.

This means you never have counterparty risk on an exchange-traded option. Whether you’re holding a credit spread or a straddle, the OCC guarantees settlement. It’s one of the structural advantages of exchange-traded options over OTC (over-the-counter) derivatives — and it’s something most traders take for granted without understanding how fundamental it is to market stability.

How Structure Shapes Your Daily Trading

Understanding options market structure isn’t academic — it directly improves your trading decisions every session.

Strike Selection Informed by Positioning

Large open interest at specific strikes creates “gravity” effects. Market makers hedging concentrated positions at a particular strike tend to pin the underlying near that level as expiration approaches. Knowing where the largest open interest sits helps you position butterflies and avoid placing iron condors where pinning is unlikely.

Understanding Bid-Ask Spreads

The bid-ask spread isn’t random — it reflects the market maker’s cost of providing liquidity. Spreads widen when:

- Volatility is high: Hedging cost increases, so market makers charge more

- Near market open/close: Uncertainty is elevated in the first and last 15 minutes

- Low open interest strikes: Less competition among market makers

- Multi-leg orders: Complex orders like butterflies and condors have wider “natural” spreads because each leg has its own bid-ask

The structural insight: trade when spreads are tightest (mid-session), use limit orders that split the bid-ask, and favor high-open-interest strikes where market maker competition compresses spreads.

Reading Market Flows for Edge

Options order flow — particularly large institutional trades — provides information about how sophisticated participants are positioning. Unusual call buying, heavy put selling, or large straddle purchases all shift the options market structure by changing dealer positioning and hedging requirements.

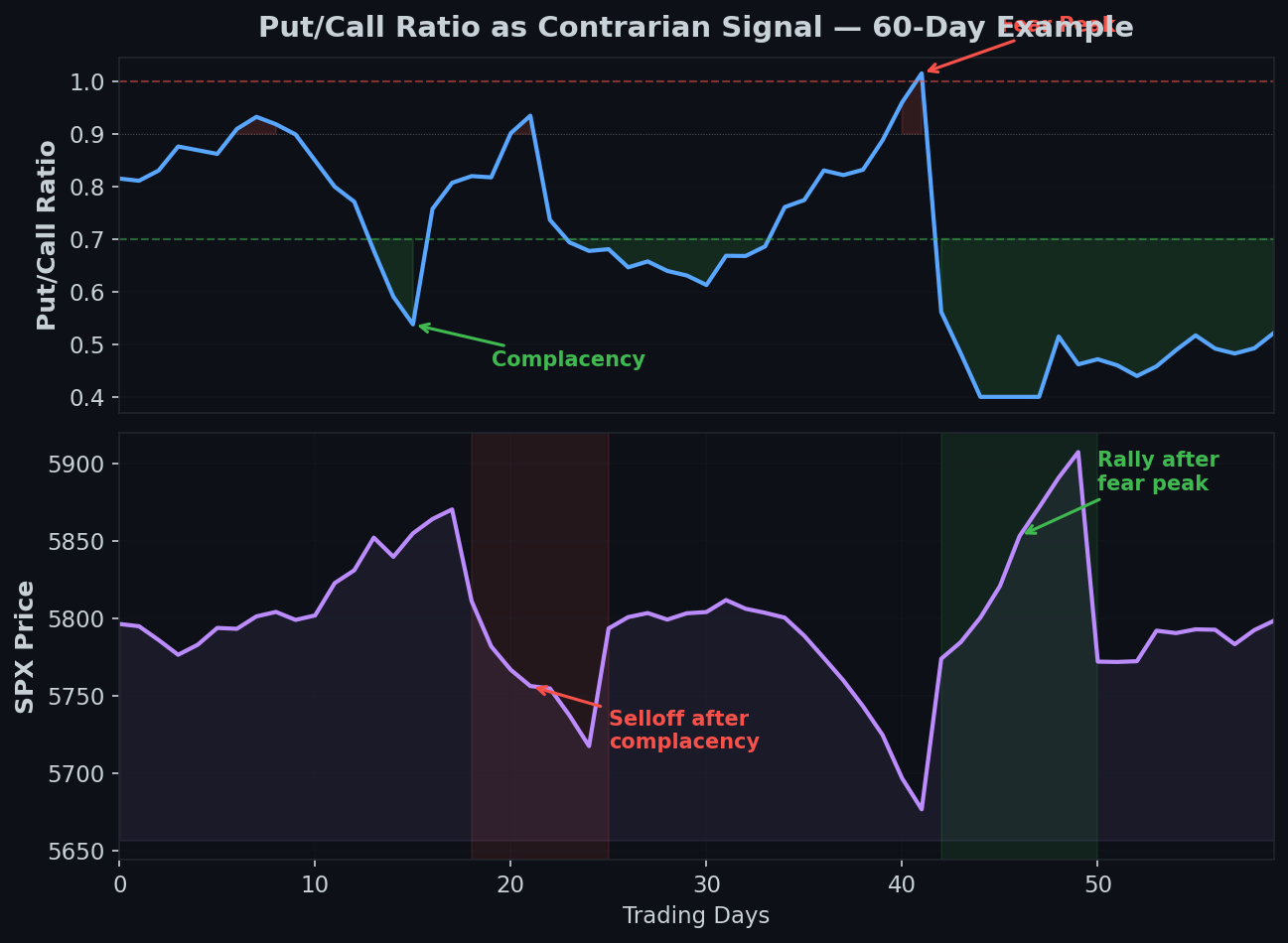

Tools like GEX analysis, put/call ratios, and volume-weighted open interest give you a window into these structural flows. They don’t predict direction — but they tell you the current structural environment, which informs how aggressively to trade and which strategies have the highest edge in that regime.

Why Structure Matters More Than Strategy

A debit spread that’s profitable in a positive-gamma, low-VIX environment can be a consistent loser in a negative-gamma, elevated-VIX regime — even with identical entry criteria. The strategy didn’t change. The structure did.

The Greeks on your position tell you what you’re exposed to. The market structure tells you what forces are acting on those exposures. Delta tells you your directional risk. GEX tells you whether the structural environment will amplify or dampen that directional move. IV crush tells you what happens to your vega. The term structure tells you where the market expects volatility to go.

Mastering options market structure means graduating from “I know what my trade does” to “I know what the market is likely to do to my trade.” That’s the difference between a trader who executes strategies and a trader who understands the environment those strategies operate in.

Building this structural awareness into your daily routine — checking GEX levels, monitoring the VIX regime, tracking dealer positioning — is as important as any risk management rule or strategy selection framework. The structure is the context. Without context, every trade is a guess.

Frequently Asked Questions

What is options market structure?

Options market structure refers to the ecosystem of exchanges, market makers, clearing houses, and institutional participants that determine how options are priced, traded, and settled. It encompasses order execution mechanics, dealer hedging behavior, the role of the OCC, and how large participant flows create structural forces that drive price action in the underlying market.

How do market makers affect options prices?

Market makers continuously post bids and offers across thousands of strikes, profiting from the bid-ask spread. Their hedging activity — buying or selling the underlying to remain delta-neutral — creates mechanical flows that either suppress or amplify volatility depending on whether they are collectively long or short gamma. This is the basis of gamma exposure analysis.

Why are SPX put options more expensive than calls?

SPX puts are structurally more expensive because institutional hedgers (pension funds, mutual funds, insurance companies) create persistent demand for downside protection. This demand pushes put implied volatility above call IV, creating the volatility skew. It reflects structural hedging behavior rather than directional sentiment.

What role does the OCC play in options trading?

The Options Clearing Corporation acts as the central counterparty for all exchange-traded options in the United States. It guarantees settlement on both sides of every trade, eliminating counterparty risk. When you hold an SPX option position, the OCC ensures you receive payment at settlement regardless of the financial condition of the trader on the other side.

How does 0DTE trading impact market structure?

The growth of 0DTE options trading has concentrated massive gamma exposure at near-term strikes, requiring market makers to hedge in real time throughout each session. This creates more pronounced intraday volatility patterns, stronger pin effects near large open interest strikes, and amplified moves when gamma flips from positive to negative. Daily notional volume regularly exceeds one trillion dollars.