SPX options are the professional standard for trading the S&P 500. Whether you’re placing 0DTE butterflies, selling credit spreads, or hedging a portfolio, SPX options offer structural advantages that stock and ETF options simply can’t match — cash settlement, European-style exercise, and 60/40 tax treatment under Section 1256.

This guide covers everything you need to know about SPX options: how they work, when they trade, how the option chain is structured, and why serious options traders choose SPX over alternatives like SPY.

What Are SPX Options?

SPX options are index options based on the S&P 500 index. You cannot buy or sell “shares” of SPX — it’s a calculated index value, not a tradable security. These are your only way to trade options directly on the S&P 500 index itself.

These options are listed and traded on the CBOE (Chicago Board Options Exchange), which has exclusive listing rights. They are among the most liquid options contracts in the world, with daily volume regularly exceeding one million contracts.

Key characteristics:

- European-style exercise — can only be exercised at expiration, never before

- Cash-settled — no shares change hands; profits and losses are settled in cash

- Section 1256 tax treatment — 60% long-term / 40% short-term capital gains regardless of holding period

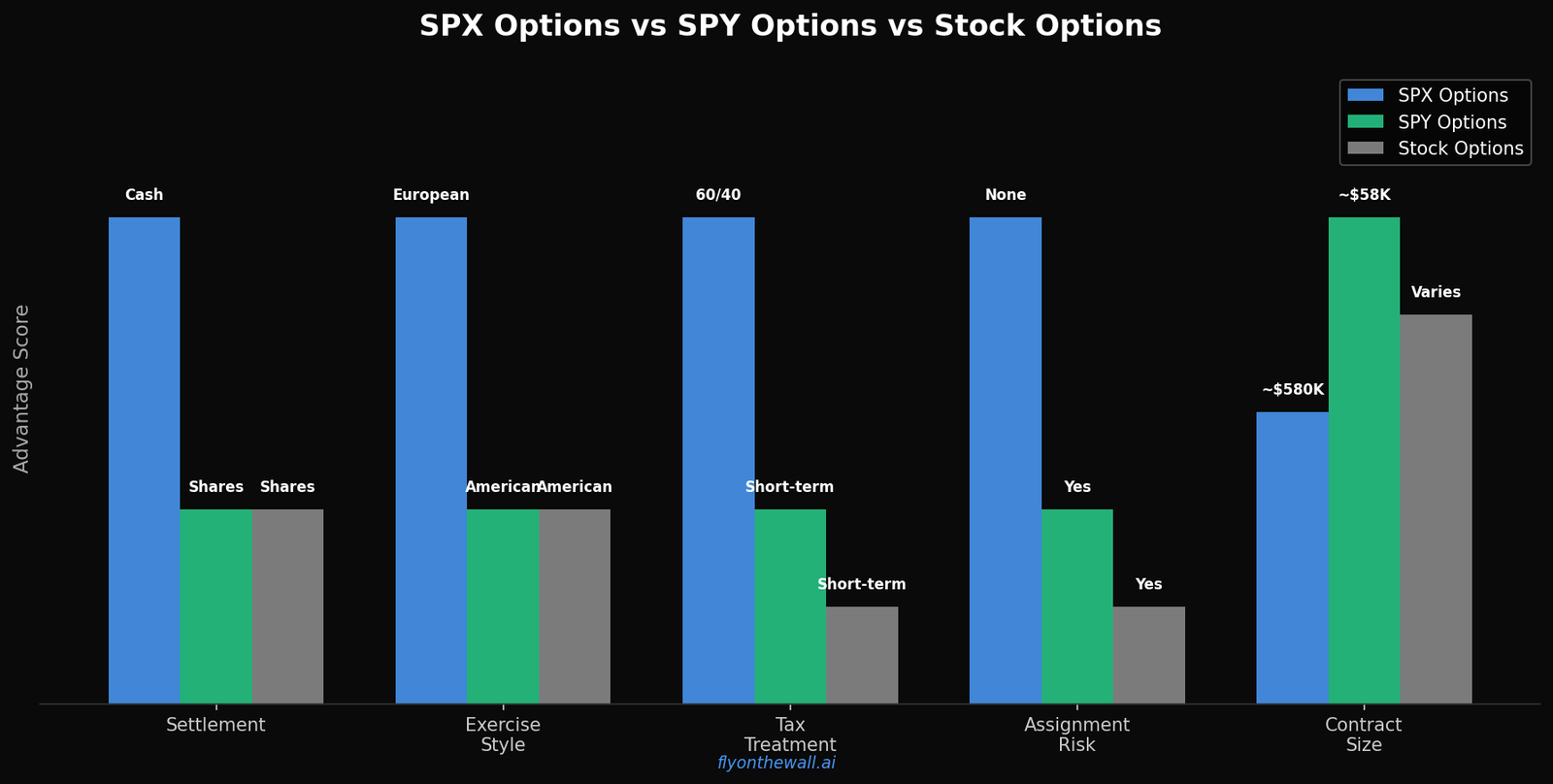

- Large notional size — with SPX around 5,800, each contract controls roughly $580,000 in notional exposure

These contracts are not the same as SPY options. SPY is an ETF that tracks the S&P 500, but SPY options are equity options with completely different settlement, exercise, and tax rules. For a detailed comparison, see our breakdown of the key differences between the two instruments.

Key Differences from Stock and ETF Options

If you’ve only traded equity options — calls and puts on individual stocks or ETFs — these index contracts work differently in several important ways.

No shares to deliver. When a stock option expires in the money, shares get transferred. When an SPX option expires in the money, you receive cash equal to the intrinsic value. There are no shares of SPX to deliver because SPX is an index, not a security.

No early assignment. Stock options (American-style) can be exercised at any time before expiration. these contracts (European-style) can only be exercised at expiration. This is critical for multi-leg strategies — your short legs cannot be assigned early, which means butterfly spreads and iron condors stay intact until settlement.

Multiplier is 100. Like equity options, each contract has a 100 multiplier. A $1.50 premium costs $150 per contract. A 10-wide butterfly with a $0.50 debit costs $50 per contract.

Settlement can be AM or PM. Standard monthly contracts (third Friday expiration) use AM settlement — the opening prices on expiration morning determine the settlement value. Weekly and daily expirations (SPXW) use PM settlement — they settle at the closing price. This distinction matters and catches traders off guard if they’re not aware.

Reading the Option Chain

The SPX option chain can look overwhelming at first glance. Multiple expiration cycles run simultaneously, and the number of available strikes is enormous. Here’s how to navigate it.

Expiration types:

- Standard monthly (SPX) — third Friday of each month, AM-settled. These are the original SPX options.

- Weekly (SPXW) — expire every Friday, PM-settled. Introduced to meet demand for shorter-dated exposure.

- Daily (SPXW) — expire Monday through Friday, PM-settled. These are the 0DTE contracts that have transformed options trading since their introduction.

In your broker’s option chain, you’ll see both “SPX” and “SPXW” designations. The key difference is settlement — AM for standard monthlies, PM for everything else. When trading 0DTE, you’re always in the SPXW chain.

Strike price intervals: The chain offers strikes at 5-point intervals near the money and 25-point intervals further out. During active trading sessions, the at-the-money strikes have the deepest liquidity with penny-wide bid-ask spreads.

Volume and open interest: On a typical trading day, the at-the-money and near-the-money strikes in the 0DTE chain show the highest volume. Open interest builds in the weekly and monthly chains. When reading the option chain, focus on volume for intraday liquidity and open interest for swing positions.

Implied volatility across the chain: These contracts exhibit a pronounced volatility skew — out-of-the-money puts carry higher implied volatility than equidistant calls. This skew reflects the market’s demand for downside protection and directly affects strategy pricing. Butterflies, for instance, are cheaper when placed above the current price than below it due to this skew.

SPX Options Trading Hours

Knowing when these contracts trade — and when they don’t — prevents costly mistakes.

Regular trading hours: 9:30 AM to 4:00 PM Eastern Time, matching the New York Stock Exchange session. This is when the vast majority of volume occurs.

Extended hours: There is also a Global Trading Hours (GTH) session from 8:15 PM to 9:15 AM Eastern (Sunday through Friday). Volume during extended hours is significantly lower, spreads are wider, and liquidity is thinner. Most retail traders should avoid this session unless hedging overnight risk.

Settlement timing:

- AM-settled (standard monthly) — settlement value is calculated from opening prices on expiration Friday morning. Trading in the expiring series stops at market open.

- PM-settled (weekly/daily) — settlement value is the closing price at 4:00 PM ET. You can trade until the close.

For 0DTE trading, the PM settlement is what matters. Your daily expiration options settle at the 4:00 PM close, giving you the full trading session to manage positions.

Settlement and Exercise Style

Settlement is where these contracts diverge most from equity options, and where they provide their biggest structural advantage.

Cash settlement in practice: If you hold a long 5800 call and SPX settles at 5810, you receive $1,000 in cash (10 points × $100 multiplier). No shares, no margin calls, no aftermarket surprises. The cash hits your account the next business day.

European-style exercise: Your contracts cannot be exercised before expiration. This means if you’re short the 5800 call as part of a butterfly or iron condor, nobody can exercise against you early — even if SPX is 50 points through your strike. The position stays intact. For anyone trading multi-leg strategies, this is the single most important structural feature.

Assignment risk is zero. Because exercise only happens at expiration and settlement is cash, there is no assignment risk at any point during the life of the trade. Compare this to SPY options, where early assignment can blow up a perfectly hedged position at any time.

The 60/40 Tax Advantage

These index contracts qualify as Section 1256 under the IRS code. This provides two significant tax advantages over equity options.

60/40 tax treatment: Regardless of how long you hold the position — even a 0DTE trade held for four hours — gains are taxed as 60% long-term capital gains and 40% short-term capital gains. For a trader in the 35% federal bracket, the blended rate is approximately 26%, compared to 35% for short-term equity option gains.

On $50,000 in annual trading profits, that’s roughly $4,500 in tax savings per year — just from choosing SPX over equity options like SPY.

Simplified reporting: Section 1256 contracts are reported on IRS Form 6781 using mark-to-market accounting. You don’t need to calculate individual holding periods for each trade. Your broker provides the net gain or loss, you report it on one form, and you apply the 60/40 split. For active traders placing dozens of trades per week, this saves significant time at tax filing.

Using Historical Chain Data

Historical option chain data reveals patterns that real-time data alone cannot show.

Why it matters: Historical chain data shows you how implied volatility behaved around specific events, how quickly time decay accelerated in 0DTE chains, and where institutional volume concentrated. This context is what separates informed butterfly placement from guessing.

What to look for:

- Volume patterns — which strikes consistently attract the most volume at different points in the session

- Implied volatility trends — how IV behaves in different VIX regimes across the 0DTE chain

- Open interest shifts — large open interest builds that indicate institutional positioning or dealer hedging levels

- Historical settlement values — where SPX actually closed relative to the day’s range, useful for calibrating butterfly placement zones

Where to access it: The CBOE provides delayed historical data. Professional-grade historical option chain data is available through data vendors like ORATS, OptionMetrics, and Polygon.io. Most brokers offer limited historical chain views within their platforms.

Best Strategies for Trading SPX Options

These contracts support every options strategy, but certain structures benefit most from SPX’s unique characteristics.

0DTE butterfly spreads are the signature strategy for this instrument. Cash settlement means no assignment risk on the short legs, European exercise keeps multi-leg positions intact, and the concentrated daily-expiration liquidity keeps spreads tight. A typical 10-wide SPX butterfly costs $40-$150 in debit with a potential return of 5-25x. For the complete framework including VIX regime width selection and profit management, see our practitioner’s guide to 0DTE butterfly spreads.

Credit spreads and iron condors benefit from European-style exercise — your short legs can’t be assigned early, eliminating the position-blowing risk that equity options carry. The 60/40 tax treatment also applies to premium collected, making SPX credit strategies more tax-efficient than equivalent SPY trades.

Portfolio hedging with SPX put options provides direct exposure to the S&P 500 index without the tracking error of ETF-based hedges. Institutional portfolio managers use SPX puts as their primary hedging instrument for this reason.

Calendar and diagonal spreads work well in SPX because the multiple simultaneous expiration cycles (daily, weekly, monthly) give you precise time spread construction that isn’t available in most equity options.

Regardless of strategy, These contracts reward traders who understand the structural advantages and use them intentionally — not as a substitute for SPY, but as a fundamentally different instrument built for serious options trading.

Frequently Asked Questions

What are SPX options and how do they work?

SPX options are European-style, cash-settled index options on the S&P 500. You cannot buy shares of SPX — only trade options on the index value. When an SPX option expires in the money, the profit is paid in cash. There is no share delivery and no assignment risk. SPX options qualify for Section 1256 tax treatment with a 60/40 long-term/short-term capital gains split.

What time can you trade these contracts?

These contracts trade during regular market hours from 9:30 AM to 4:00 PM Eastern Time. An extended Global Trading Hours session runs from 8:15 PM to 9:15 AM Eastern, Sunday through Friday. Most volume and liquidity is concentrated during regular hours. Daily 0DTE expirations settle at the 4:00 PM close.

Are SPX options cash-settled?

Yes. All SPX options are cash-settled. When an option expires in the money, the holder receives the cash difference between the strike price and the settlement value of the index. No shares are exchanged. This eliminates assignment risk entirely, which is particularly valuable for multi-leg strategies like butterflies and iron condors.

What is the difference between SPX and SPXW options?

SPX refers to the standard monthly options that expire on the third Friday of each month using AM settlement — the settlement value is calculated from opening prices on expiration morning. SPXW refers to weekly and daily expiration options that use PM settlement — they settle at the 4:00 PM closing price. For 0DTE trading, you are always trading SPXW contracts.

Can you trade SPX options in a small account?

Yes. While SPX has a large notional value (around $580,000 per contract), defined-risk strategies like butterfly spreads cost as little as $40-$150 per trade. A $5,000 account can comfortably trade SPX butterflies. For accounts under $5,000, SPY options offer 1/10th the contract size for more granular position sizing, though you lose the tax and settlement advantages of SPX.

Start Trading With Structure

SPX is the instrument. Structure is what turns it into consistent results. At Fly on the Wall, we trade every session with real capital — live setups, VIX regime analysis, and a discipline framework built for the realities of 0DTE trading.

Start with the Observer for real-time tools and daily market analysis. Step up to Activator for full execution tools and weekly coaching. Or go all-in with Navigator for daily direct coaching. Compare all plans here.