0DTE options — zero days to expiration — are options contracts that expire on the same day you trade them. You buy them in the morning. They settle by the close. Whatever happens in between is the entire life of the trade.

This is not a niche corner of the market. 0DTE contracts now account for over 40% of all SPX options volume on any given day. Institutional desks trade them. Market makers hedge with them. And a growing number of retail traders have figured out that same-day expiration changes the fundamental math of options trading — not because it’s faster, but because it strips away the variables that make longer-dated options unpredictable.

This guide covers how these contracts work, why they behave differently from everything else in the options chain, and how structural traders use them to position with defined risk and asymmetric reward.

How 0DTE Options Work

Every options contract has an expiration date. Most traders think in terms of weeks or months. 0DTE options expire today — the same day you open the position.

On SPX, these are SPXW contracts (weekly/daily series) that use PM settlement. That means the settlement value is the closing price at 4:00 PM Eastern. You have the full trading session to open, manage, and close positions.

The mechanics that matter:

- Cash-settled — no shares change hands. Profit or loss is paid in cash at settlement.

- European-style exercise — contracts can only be exercised at expiration. Your short legs cannot be assigned early, which keeps multi-leg structures intact all day.

- Section 1256 tax treatment — 60% long-term / 40% short-term capital gains, regardless of holding period. Even a four-hour trade gets this treatment.

- Rapid time decay — theta accelerates dramatically on the final day. Options lose extrinsic value throughout the session, which is either your enemy or your edge depending on how you structure the trade.

For a deeper look at the instrument itself, see our complete guide to SPX options, which covers the option chain, settlement mechanics, and trading hours in detail.

Why Same-Day Expiration Changes the Math

Longer-dated options carry uncertainty you cannot control. Overnight risk. Weekend gaps. Earnings surprises. Fed announcements that happen between sessions. Every night you hold a position, you are exposed to events that have nothing to do with your trade thesis.

0DTE contracts eliminate overnight risk entirely. Your trade opens and closes within a single session. The only variable is what happens during market hours — and that variable is exactly what structural tools are designed to read.

This changes three things:

Time decay works in hours, not days. On a 30-day option, theta burns slowly. On a same-day contract, theta is a freight train. An at-the-money option that costs $4.00 at the open might be worth $0.20 by 3:30 PM if price hasn’t moved. Structures that benefit from decay — like butterfly spreads — thrive in this environment.

Gamma is amplified. With zero time remaining, small price moves create large changes in delta. This is why same-day contracts can produce outsized returns on relatively small price movements. A 10-point SPX move that barely registers on a monthly option can double or triple the value of a well-placed daily butterfly.

Implied volatility resets every day. Each morning is a clean slate. You are not carrying the baggage of a position that went against you yesterday. Every session is a new structural read, a new setup, and a new defined-risk entry.

The Structural Approach to 0DTE Trading

Most traders who fail at 0DTE options do so because they treat these contracts like lottery tickets. Pick a direction, buy a cheap option, hope it moves. That approach has a predictable outcome: you lose most of the time.

The structural approach is fundamentally different. Instead of predicting where price will go, you read where the market is positioned — then place trades that profit when the structure resolves.

Three structural layers matter before every session:

Dealer positioning and gamma exposure. Market makers hold enormous options positions that force them to hedge. When dealers are short gamma, their hedging amplifies price moves. When they are long gamma, their hedging dampens moves. Knowing which regime you are in before the open determines everything — your strategy selection, your width, and your position size.

Volume profile and liquidity structure. Where did real volume trade yesterday? Which high-volume nodes act as magnets? And what gaps does price move through quickly? Volume profile shows you the structural support and resistance that price charts alone cannot reveal.

VIX regime context. The VIX tells you the implied volatility environment for the session. Different VIX levels demand different approaches. A session with VIX at 14 is a different market than a session with VIX at 28 — and your trade construction should reflect that difference explicitly.

At Fly on the Wall, these layers are surfaced in real time through tools like the Market Mode Score, Dealer Gravity, and the GEX + Volume Profile overlay. The platform was built specifically because these structural reads were impossible to assemble manually from six different tools before the open each day.

0DTE Strategies That Actually Work

Not every options strategy translates to same-day expiration. Some thrive. Some quietly destroy accounts. Here is what the structural data actually shows.

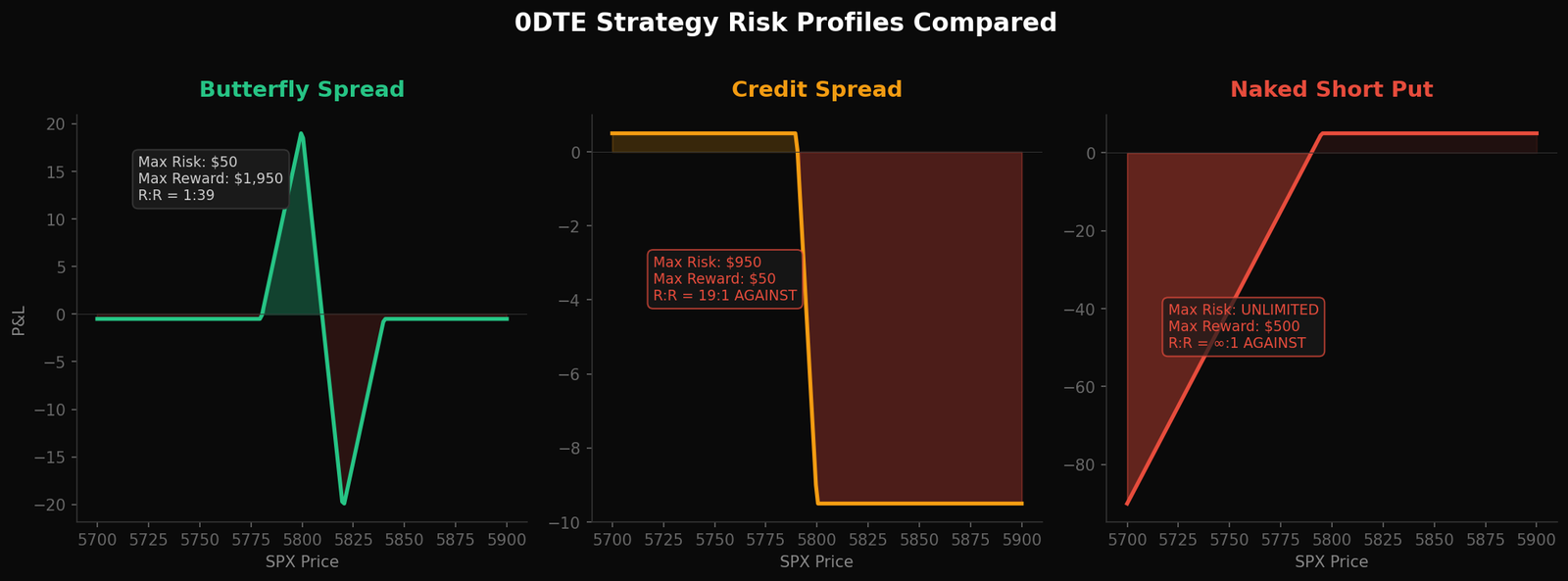

Butterfly spreads are the signature strategy for 0DTE trading. A defined-risk structure that costs $40-$150 per contract with potential returns of 5-25x. You know your maximum loss before you enter. European-style exercise keeps the structure intact all day. And the concentrated theta decay of same-day expiration is exactly what makes the butterfly payoff profile work. For the complete framework including VIX regime width selection and profit targets, see our practitioner’s guide to butterfly spreads.

Credit spreads are the most popular retail strategy — and the most dangerous for same-day trading. A typical credit spread collects $0.50 in premium and risks $9.50. That is a 19:1 adverse risk-to-reward ratio. One bad session wipes out weeks of small wins. The math does not improve with experience. It gets worse, because the losses are always larger than the wins.

Iron condors require static, range-bound conditions. On a day with VIX above 20, the probability of SPX staying within a narrow range for the entire session is low. Iron condors work in textbook examples. They fail in live markets where regime shifts happen intraday.

Naked options and straddles carry undefined risk. In a same-day context where gamma is amplified, a directional move against a naked position can produce catastrophic losses within hours. There is no overnight gap to blame — the loss happens in real time while you watch.

The structural evidence is clear: defined-risk, asymmetric structures outperform open-risk premium collection on a risk-adjusted basis. This is not opinion. It is the measurable outcome of choosing strategies that survive their worst day.

Risk Management for Same-Day Expiration

Risk management for 0DTE options is simpler than most traders expect — because the structure itself defines the risk.

Define your risk before entry. A butterfly spread costs $0.50 per contract. That is your maximum loss. There is no stop-loss to set, no margin call to worry about, and no gap risk overnight. The risk was defined the moment you entered the trade.

Size by R-multiple, not by contract count. If your risk unit is $100 per trade, a $50 butterfly lets you take two contracts. A $150 butterfly means one contract. The number of contracts is a consequence of the risk unit, not the other way around.

Manage profit, not loss. This is the part most traders get backwards. On a defined-risk trade, there is nothing to manage on the downside — you already defined it. Management means taking profit at your target levels: 75-200% is common, 200-500% is strong, and anything above 500% is a runner that you let work while trailing.

Accept the loss rate. A well-structured butterfly strategy wins 45-65% of the time depending on the volatility regime. That means you lose 35-55% of the time. This is not a flaw in the strategy. It is the strategy. Your edge comes from the asymmetry — the winners are larger than the losers, and the losses are capped.

The VIX Regimes That Shape Every Session

Every trading session falls into one of three structural regimes, determined by the VIX level at the open. Each regime demands a different approach to trade construction.

Zombieland (VIX at or below 17). Low volatility. Compressed ranges. Premium is cheap. Butterflies should be narrower — 10-wide is typical. The market tends to grind, not move. Patience is the edge. In this environment, the structure usually holds, and butterflies placed near the expected value zone have the highest probability of profit.

Goldilocks (VIX between 17 and 32). Moderate volatility. This is where most trading sessions live. Ranges are wider, premium is fair, and directional moves are possible but not guaranteed. Butterfly width expands to 15-20 wide. This is the regime where structural reads matter most — where dealers are positioned determines whether the session grinds or breaks.

Chaos (VIX above 32). High volatility. Large intraday ranges. Premium is expensive. Butterflies need to be wider — 20-30 wide — and position size should be reduced. However, this is also where the largest asymmetric payoffs occur. A well-placed butterfly in a chaos session can return 10-25x the risk. The key is sizing small enough to survive the sessions where it does not work.

Understanding which regime you are trading 0DTE options in before the open is not optional. It is the first decision of the day, and every subsequent decision depends on it.

Common Mistakes That End 0DTE Careers

These are not theoretical warnings. These are the patterns that consistently end 0DTE options careers — the mistakes that appear in the trading records of people who quit.

Trading without a structural read. Opening a position because price “looks like” it is going up is not a thesis. It is a guess. Every trade should begin with a regime assessment, a structural read, and a scenario ranking — in that order.

Using the wrong width for the regime. A 10-wide butterfly in a VIX 30 environment is too narrow. A 25-wide butterfly in Zombieland is too wide and too expensive. The width must match the regime. There is no single correct width.

Chasing after the move. If SPX has already moved 30 points and you are entering a butterfly in the direction of the move, you are buying a structure at the worst possible time. The structural edge exists before the move, not after.

Setting stop losses on defined-risk trades. If your maximum risk is $50 and you set a stop at $25, you have cut your risk in half — but you have also eliminated the scenario where the trade recovers. The whole point of defined risk is that you sized the trade to accept the full loss. Stops on butterflies destroy the edge.

Sizing too large. If losing a trade changes your emotional state, you are too large. The correct position size is the one where a maximum loss is boring. Not painful. Not frustrating. Boring.

0DTE Options vs Traditional Options

The differences between same-day and longer-dated options are not just about time. They are structural.

Same-day contracts settle in hours, not weeks. There is no overnight risk. Gamma is at its peak, which means small price moves produce large changes in option value. Time decay is accelerated, making theta either your greatest ally or your fastest drain.

Traditional options carry overnight and weekend risk. They move more slowly. Gamma is lower, so price moves have a more muted effect on option value. And they require monitoring across multiple sessions, which introduces decision fatigue and emotional exposure.

For traders who have compared both approaches, the distinction is clear: same-day expiration rewards structural precision while longer-dated options reward patience and directional conviction. Neither is better in absolute terms. But if your edge is reading market structure — dealer positioning, gamma exposure, liquidity — then the same-day format lets you express that edge with zero overnight risk.

Frequently Asked Questions

What does 0DTE mean in options trading?

0DTE stands for “zero days to expiration.” It refers to options contracts that expire on the same day they are traded. On SPX, these are SPXW contracts with PM settlement at the 4:00 PM Eastern close. The trade opens and closes within a single market session, eliminating overnight risk entirely.

Are 0DTE options risky?

The risk depends entirely on the strategy. Undefined-risk strategies like naked puts or straddles can produce catastrophic losses in hours. Defined-risk strategies like butterfly spreads cap your maximum loss at the debit paid — typically $40-$150 per contract. The instrument is not inherently risky. The structure you choose determines the risk.

How much money do you need to trade 0DTE options?

A defined-risk butterfly spread on SPX can cost as little as $40-$150 per contract. A $5,000 account can comfortably trade same-day butterflies with proper position sizing. For accounts under $5,000, SPY options offer 1/10th the contract size, though you lose the cash settlement and tax advantages of SPX.

What is the best strategy for 0DTE options?

Butterfly spreads offer the best risk-adjusted profile for same-day expiration trading. They provide defined risk, asymmetric reward (5-25x potential), and benefit from the accelerated time decay that characterizes same-day contracts. Credit spreads and iron condors carry adverse risk-to-reward ratios that compound losses over time.

Can you trade 0DTE options every day?

Yes. SPX daily expirations (SPXW) are available Monday through Friday. Each session is a clean slate with a new structural setup. However, not every session presents a high-quality setup. The discipline to sit out weak structure days is as important as the ability to trade strong ones.

Start Reading the Structure

Every session, the market tells you where it is positioned — before price moves. Dealer flow, gamma exposure, liquidity structure, VIX regime. The information is there. The question is whether you can see it.

Fly on the Wall was built to surface that structural picture in real time. Start with the Observer for daily structural analysis and the tools that show you where the market is positioned before the open. Step up to Activator for full execution tools, GEX overlay, and weekly coaching. Or go all-in with Navigator for daily direct coaching with Ernie. Compare all plans here.