Time decay in options is the constant, silent cost of holding a position. Every contract you own loses value with every passing hour — not because the market moved against you, but because time moved forward. Understanding how time decay options pricing works is the difference between a trader who accounts for the cost of time and one who watches premium evaporate without knowing why.

Most traders learn that theta exists, nod, and move on. They treat it as a line item on their Greeks dashboard. But time decay is not a passive statistic. It is the single largest structural force in short-dated options — especially 0DTE contracts where a position can lose half its value in ninety minutes without the underlying moving a single point. This guide explains how time decay options pricing actually works, why it accelerates the way it does, and how to position yourself on the right side of it.

What Is Time Decay in Options?

Time decay is the reduction in an option’s extrinsic value as it approaches expiration. Every option has two components of value: intrinsic value (how far it is in the money) and extrinsic value (the premium above intrinsic, driven by time remaining and implied volatility). Time decay erodes the extrinsic portion. It does not touch intrinsic value.

The Greek that measures this is theta — expressed as the dollar amount an option loses per day, all else equal. A theta of -0.50 means the option loses fifty cents of value every day purely from the passage of time. The “all else equal” qualifier matters enormously: in practice, delta, gamma, and vega are also shifting, which means theta rarely acts in isolation. But its cumulative effect over hours and days is the baseline cost of holding any option.

Time decay exists because options are wasting assets. They have an expiration date — as the OCC’s options pricing reference explains, every contract’s premium reflects the probability of ending in the money, and that probability shrinks as time passes. A stock can sit in your portfolio indefinitely, but an option has a countdown clock. The market prices this countdown into the premium, and as that clock ticks down, the premium shrinks — not linearly, but on an accelerating curve that catches many new traders off guard.

Why Theta Accelerates Near Expiration

The most important characteristic of time decay options traders must understand is its non-linear acceleration. A 30-day option might lose $2 of extrinsic value over its first 15 days and $8 over its final 15 days. The decay curve is roughly proportional to the square root of time remaining — which means the last few days (and especially the last few hours) are where the majority of theta burn occurs.

This acceleration has practical consequences. Holding a weekly option over the weekend costs more in theta than holding a 60-day option over the same weekend, even if the options have similar extrinsic value. For 0DTE traders, this acceleration is the defining feature of the instrument — theta is not a background cost, it is the primary force acting on every position from the opening bell.

The math behind this acceleration comes from the Black-Scholes model, where extrinsic value is proportional to the square root of time. Cut the time to expiration in half, and extrinsic value drops by about 29% (not 50%). Cut it to one quarter, and extrinsic value drops by 50%. This square-root relationship means the rate of decay accelerates as time shrinks — the same way a ball rolls faster as it approaches the bottom of a hill.

How Theta Interacts with Delta, Gamma, and Vega

Theta does not operate in a vacuum. It exists in constant tension with the other Greeks, and understanding those interactions is what separates textbook knowledge from practical trading skill.

Theta and delta: At-the-money options have the highest theta because they have the most extrinsic value to lose. Deep in-the-money options have little extrinsic value (they are mostly intrinsic), so their theta is low. Far out-of-the-money options also have low absolute theta, but their entire value is extrinsic — so while the dollar amount of daily decay is small, it represents a larger percentage of the option’s total value. A $0.50 OTM option losing $0.05 per day is decaying at 10% daily.

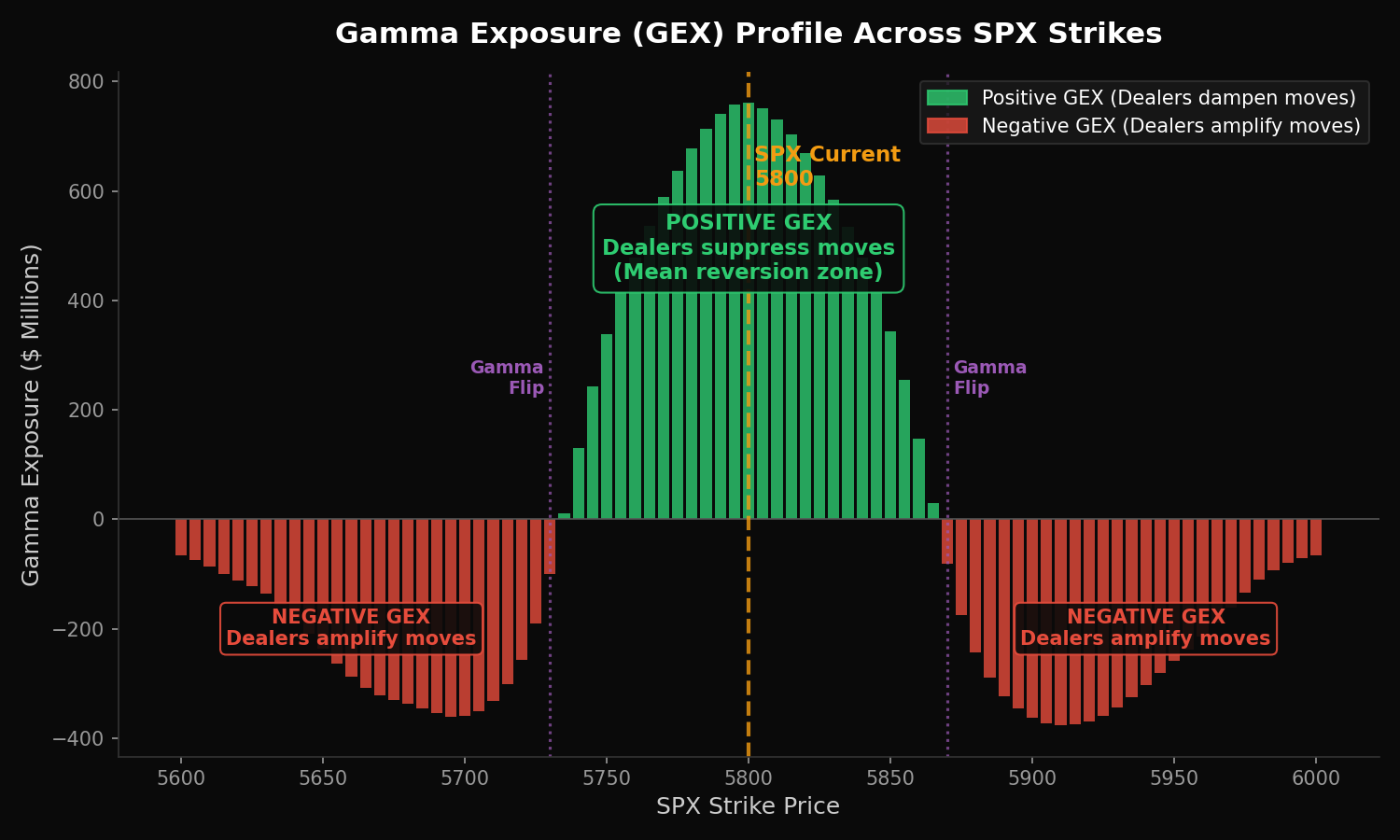

Theta and gamma: These two Greeks have an inverse relationship that is critical for 0DTE trading. High gamma means the option’s delta changes rapidly with price movement — which creates the potential for large gains. But high gamma is paid for with high theta. This is the fundamental tradeoff in short-dated options: the same conditions that make a position responsive to price movement also make it expensive to hold. Gamma exposure analysis helps identify when this tradeoff favors buyers versus sellers.

Theta and vega: When implied volatility rises, extrinsic value increases — which temporarily offsets theta decay. When IV drops (the IV crush after an earnings announcement or economic release), extrinsic value collapses and theta’s effect is compounded. For time decay options trading, understanding the volatility environment is essential because it determines whether theta is working at normal speed or whether IV changes are amplifying or masking it.

How to Calculate Theta Cost on Your Positions

Calculating time decay options costs on your own positions is straightforward but requires attention to what the numbers actually mean.

Reading theta from your platform: Every options platform displays theta as a per-day figure. If you hold a call with theta of -0.35, you can expect approximately $35 of time decay per contract per day (since each contract represents 100 shares). But this is an approximation based on current conditions — theta itself changes throughout the day as gamma shifts, IV fluctuates, and time passes.

Intraday theta for 0DTE positions: For same-day expirations, the daily theta figure understates the reality because decay is concentrated in the trading session. A 0DTE option at 9:30 AM might show theta of -$2.00, but the actual decay from 9:30 to 4:00 is the entire remaining extrinsic value — which could be $5.00 or more. The standard theta metric assumes 365 calendar days, so for a position that expires in 6.5 hours, the actual hourly decay rate is far higher than the daily figure implies.

Portfolio-level theta: If you hold multiple options positions, your net theta tells you the aggregate daily cost of time. A portfolio with net theta of -$150 is paying $150 per day for the privilege of holding those positions. This number should be checked against your expected daily P&L from delta and gamma moves. If your theta cost exceeds your realistic daily gain from price movement, you are structurally paying more for time than you are likely to earn from direction.

Strategies That Use Time Decay to Your Advantage

The strategic question with time decay is not whether it exists — it always does. The question is whether you are paying it or collecting it, and whether that positioning matches the current market regime.

If you have been following the FOTW educational framework and applying it in live sessions, you have seen how structural analysis transforms time decay from a background cost into a positioning tool. The daily pre-market analysis in Observer ($17/week) covers the exact conditions — GEX regime, expected move, VIX level — that determine which side of theta you want to be on for each session. Activator ($97/month) adds real-time GEX tools and weekly coaching, while Navigator ($267/month) provides daily direct coaching with Ernie. Compare all plans here.

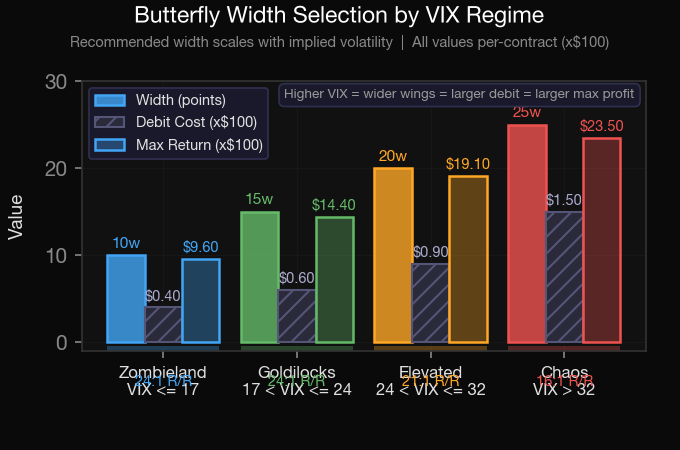

Buying structures with defined risk: Butterfly spreads are the most theta-efficient buying structure. You pay time decay on the long legs but collect it on the short legs, resulting in a net theta that is far lower than a naked long call or put. A butterfly centered at a dealer gravity level uses time decay constructively — as expiration approaches, if price converges on the target, the butterfly’s value increases even as theta erodes the outer legs. The structure turns time decay from an enemy into an ally.

Credit spreads and iron condors: Credit spreads and iron condors collect theta directly — you receive premium upfront and profit as time decay erodes the value of the options you sold. These strategies are positive theta, meaning time working in your favor. However, they carry negative gamma risk: a sharp move against the position creates losses that accelerate. The tradeoff is the mirror image of buying options.

The structural approach: Rather than categorically buying or selling time, structural traders read the positioning landscape first. In positive GEX environments with a narrow expected move, selling premium (collecting theta) is favored because dealer hedging suppresses volatility. In negative GEX environments with an expanded expected move, buying defined-risk structures (paying controlled theta) is favored because directional moves are more likely. The VIX regime provides additional context — high VIX means premium is expensive (favorable for sellers), while low VIX means premium is cheap (less costly for buyers).

Common Theta Mistakes That Cost Real Money

The most expensive time decay options errors are not mathematical. They are behavioral — holding positions without accounting for the cost of time.

Holding long options through low-volatility sessions. If the market is compressing in a positive GEX environment, your long calls or puts are decaying every hour without directional movement to offset them. The right response is not to hold and hope — it is to recognize before the session starts that the positioning landscape does not favor directional buying, and to either sit out or use a structure with lower net theta.

Ignoring theta on multi-day holds. Holding options over a weekend or through a holiday costs two to three days of theta with no opportunity for price movement to compensate. For weekly options, this weekend decay can represent 20-30% of the remaining extrinsic value. If your thesis needs more time, consider rolling to a later expiration rather than absorbing the accelerated decay.

Focusing on dollar theta instead of percentage theta. A $10 option losing $0.50 per day (5% daily decay) is in a fundamentally different situation than a $0.50 option losing $0.05 per day (10% daily decay). The dollar amount is smaller, but the rate of decay is twice as fast. OTM options near expiration can lose 20-50% of their value in a single session — a decay rate that makes profitable long-side trading nearly impossible without precise timing.

Selling premium without understanding gamma risk. New traders learn that selling options “makes theta work for you” and start selling premium aggressively. What they miss is that selling premium also sells gamma — meaning losses accelerate during sharp moves. A credit spread that collects $2 in theta per day but faces $500 of potential loss on a 2% move is not “making time work for you.” It is taking asymmetric risk for small, steady gains. Proper risk management is essential for any theta-positive strategy.

Time Decay in 0DTE Options: The Extreme Case

Same-day expiration options represent time decay options dynamics in their most concentrated form. Everything described above applies, but the effects are compressed into a single session — making theta the dominant force rather than a background consideration.

In a 0DTE session, an at-the-money SPX option might start the day with $15 of extrinsic value. By 2:00 PM, that extrinsic value is $5. By 3:30 PM, it is $1. The entire premium melts away in six and a half hours. For buyers, this means every minute that price does not move in their favor is a minute of value destruction. For sellers, it means premium flows to them continuously — but a sharp directional move can erase weeks of collected theta in minutes.

This is why the structural approach to SPX day trading emphasizes reading the positioning landscape before every session. The question is not “should I buy or sell theta?” but “does today’s GEX profile, expected move, and VIX regime favor structures that pay theta or collect it?” The answer changes daily, and getting it right is the difference between compounding steadily and bleeding out through uncompensated time decay.

Frequently Asked Questions

What is time decay in options?

Time decay is the erosion of an option’s extrinsic value as it approaches expiration. Measured by the Greek theta, it represents the daily cost of holding an option — the amount of premium that disappears purely because time has passed. Time decay accelerates as expiration nears, with the steepest losses occurring in the final days and hours before expiration.

How do you calculate time decay on options?

Your trading platform displays theta as a per-day figure on each position. Multiply theta by 100 (for standard contracts) to get the daily dollar decay. For example, theta of -0.25 means approximately $25 of decay per contract per day. For 0DTE options, the daily theta figure understates actual decay because the full remaining extrinsic value will be lost by close — calculate your true cost by looking at extrinsic value directly.

Does time decay happen on weekends?

Time decay is priced continuously by the market, including over weekends and holidays. In practice, most of the weekend theta is priced out during Friday afternoon trading. Options held over the weekend will typically show a lower price at Monday’s open than Friday’s close, even if the underlying is unchanged. For weekly options, this weekend decay can represent 20-30% of remaining extrinsic value.

How can you profit from time decay?

You profit from time decay by selling options or using credit structures like credit spreads and iron condors, which have positive theta. Alternatively, butterfly spreads reduce net theta cost by combining long and short legs. The most effective approach reads the market structure first — selling premium when dealer positioning favors range-bound action, and buying defined-risk structures when conditions favor directional moves.

Is time decay good or bad for options traders?

Time decay is neither universally good nor bad — it depends on your position and the market conditions. It benefits sellers and hurts buyers. The structural approach does not pick sides permanently. Instead, it reads the daily positioning landscape to determine whether current conditions favor paying theta (buying structures in trending environments) or collecting it (selling premium in compressed environments).